- Latest available (Revised)

- Original (As adopted by EU)

Commission Delegated Regulation (EU) 2015/35Show full title

Commission Delegated Regulation (EU) 2015/35 of 10 October 2014 supplementing Directive 2009/138/EC of the European Parliament and of the Council on the taking-up and pursuit of the business of Insurance and Reinsurance (Solvency II) (Text with EEA relevance)

You are here:

What Version

Advanced Features

- Show Geographical Extent(e.g. England, Wales, Scotland and Northern Ireland)

- Show Timeline of Changes

More Resources

Revised version PDFs

- Revised 30/07/202048.27 MB

- Revised 01/01/202048.00 MB

- Revised 08/07/201944.91 MB

- Revised 01/01/201946.16 MB

- Revised 15/09/201740.90 MB

- Revised 09/04/201746.19 MB

- Revised 02/04/201646.19 MB

- Revised 17/01/201539.54 MB

This is a Regulation originating from the EU

This is a legislation item that originated from the EU

After exit day there will be three versions of this legislation to consult for different purposes. The legislation.gov.uk version is the version that applies in the UK. The EU Version currently on EUR-lex is the version that currently applies in the EU i.e you may need this if you operate a business in the EU.

The web archive version is the official version of this legislation item as it stood on exit day before being published to legislation.gov.uk and any subsequent UK changes and effects applied. The web archive also captured associated case law and other language formats from EUR-Lex.

Changes over time for: ANNEX XVII

Changes to legislation:

Commission Delegated Regulation (EU) 2015/35, ANNEX XVII is up to date with all changes known to be in force on or before 28 April 2024. There are changes that may be brought into force at a future date. Changes that have been made appear in the content and are referenced with annotations.

Changes to Legislation

Revised legislation carried on this site may not be fully up to date. Changes and effects are recorded by our editorial team in lists which can be found in the ‘Changes to Legislation’ area. Where those effects have yet to be applied to the text of the legislation by the editorial team they are also listed alongside the legislation in the affected provisions. Use the ‘more’ link to open the changes and effects relevant to the provision you are viewing.

Changes and effects yet to be applied to Annex XVII:

- Regulation revoked by 2023 c. 29 Sch. 1 Pt. 3

- Recital 53 Sentence 1 replacement by EUR 2016/2283 Regulation

Changes and effects yet to be applied to the whole legislation item and associated provisions

- Art. 177(2)(b) words omitted by S.I. 2019/407 reg. 11(25)(a) (This amendment not applied to legislation.gov.uk. Reg. 11(25)(39) omitted immediately before IP completion day by virtue of S.I. 2019/710, regs. 1(2), 22)

- Art. 177(2)(h)(i) words omitted by S.I. 2019/407 reg. 11(25)(b)(ii) (This amendment not applied to legislation.gov.uk. Reg. 11(25)(39) omitted immediately before IP completion day by virtue of S.I. 2019/710, regs. 1(2), 22)

- Art. 177(2)(h)(i) words substituted by S.I. 2019/407 reg. 11(25)(b)(i) (This amendment not applied to legislation.gov.uk. Reg. 11(25)(39) omitted immediately before IP completion day by virtue of S.I. 2019/710, regs. 1(2), 22)

- Art. 177(2)(r) words substituted by S.I. 2019/407 reg. 11(25)(c) (This amendment not applied to legislation.gov.uk. Reg. 11(25)(39) omitted immediately before IP completion day by virtue of S.I. 2019/710, regs. 1(2), 22)

- Art. 177(2)(s) words substituted by S.I. 2019/407 reg. 11(25)(c) (This amendment not applied to legislation.gov.uk. Reg. 11(25)(39) omitted immediately before IP completion day by virtue of S.I. 2019/710, regs. 1(2), 22)

- Art. 177(2)(t) words substituted by S.I. 2019/407 reg. 11(25)(d) (This amendment not applied to legislation.gov.uk. Reg. 11(25)(39) omitted immediately before IP completion day by virtue of S.I. 2019/710, regs. 1(2), 22)

- Art. 177(5)(a) words substituted by S.I. 2019/407 reg. 11(25)(f) (This amendment not applied to legislation.gov.uk. Reg. 11(25)(39) omitted immediately before IP completion day by virtue of S.I. 2019/710, regs. 1(2), 22)

- Art. 177(5)(c) words substituted by S.I. 2019/407 reg. 11(25)(f) (This amendment not applied to legislation.gov.uk. Reg. 11(25)(39) omitted immediately before IP completion day by virtue of S.I. 2019/710, regs. 1(2), 22)

ANNEX XVIIU.K. METHOD-SPECIFIC DATA REQUIREMENTS AND METHOD SPECIFICATIONS FOR UNDERTAKING-SPECIFIC PARAMETERS OF THE STANDARD FORMULA

A. Definitions and notations U.K.

(1)For the purpose of this Annex, the following definitions shall apply:U.K.

(a)

‘accident year’ means, with respect to a payment for an insurance or reinsurance claim, the year in which the insured event that gave rise to that claim took place;

(b)

‘development year’ means, with respect to a payment for an insurance or reinsurance claim, the difference between the year of that payment and the accident year of that payment.

(c)

‘reporting year’ means, with respect to a payment for an insurance or reinsurance claim, the year in which the insured event that gave rise to that claim was notified to the insurance or reinsurance undertaking;

(d)

‘financial year’ means, with respect to a payment for an insurance or reinsurance claim, the year in which this payment took place.

(2)For the purpose of this annex, ‘segment s’ denotes the segment for which the undertaking-specific parameter is determined, being one of the segments set out in Annex II or one of the segments set out in Annex XIV.U.K.

B. Premium risk method U.K.

Input data and method-specific data requirements U.K.

(1)The data for estimating the undertaking-specific standard deviation of segment s shall consist of the following:U.K.

(a)

the payments made and the best estimates of the provision for claims outstanding in segment s after the first development year of the accident year of those claims (aggregated losses);

(b)

the premiums earned in segment s;

Those aggregated losses and earned premiums shall be available separately for each accident year of the insurance and reinsurance claims in segment s.

(2)The following method-specific data requirements shall apply:U.K.

(a)

the data are representative for the premium risk that the insurance or reinsurance undertaking is exposed to during the following twelve months;

(b)

data are available for at least five consecutive accident years;

(c)

[F1where the premium risk method is applied to replace the standard parameters referred to in Article 218(1)(a)(ii) and (c)(ii), the aggregated losses and earned premiums are not adjusted for recoverable from reinsurance contracts and special purpose vehicles or reinsurance premiums;]

(d)

[F1where the premium risk method is applied to replace the standard parameters referred to in Article 218(1)(a)(i) and (c)(i):]

i.

the aggregated losses are adjusted for amounts recoverable from reinsurance contracts and special purpose vehicles which are consistent with the reinsurance contracts and special purpose vehicles that are in place to provide cover for the following twelve months;

ii.

the earned premiums are adjusted for reinsurance premiums which are consistent with the reinsurance contracts and special purpose vehicles that are in place to provide cover for the following twelve months;

(e)

the aggregated losses are adjusted for catastrophe claims to the extent that the risk of those claims is reflected in the non-life or health catastrophe risk sub-modules;

(f)

the aggregated losses include the expenses incurred in servicing the insurance and reinsurance obligations;

(g)

the data fit the following assumptions:

i.

expected aggregated losses in a particular segment and accident year are linear proportional in premiums earned in a particular accident year;

ii.

the variance of aggregated losses in a particular segment and accident year is quadratic in premiums earned in a particular accident year;

iii.

aggregated losses follow a lognormal distribution;

iv.

maximum likelihood estimation is appropriate.

Textual Amendments

F1 Substituted by Commission Delegated Regulation (EU) 2016/467 of 30 September 2015 amending Commission Delegated Regulation (EU) 2015/35 concerning the calculation of regulatory capital requirements for several categories of assets held by insurance and reinsurance undertakings (Text with EEA relevance).

Method specification U.K.

(3)For the purpose of paragraphs 4-6, the following notation shall apply:U.K.

(a)

accident years are denoted by consecutive numbers starting with 1 for the first accident year for which data are available;

(b)

T denotes the latest accident year for which data are available;

(c)

for all accident years, the aggregated losses in segment s in a particular accident year t are denoted by yt ;

(d)

for all accident years, the premiums earned in segment s in a particular accident year t are denoted by xt .

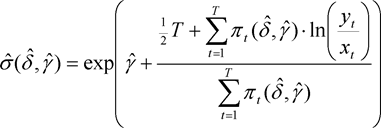

(4)The undertaking-specific standard deviation of segment s shall be equal to the following:U.K.

where:

(a)

c denotes the credibility factor set out in section G;

(e)

σ(prem,s) denotes the standard parameter that should be replaced by the undertaking-specific parameter.

(5)The standard deviation function shall be equal to the following function of two variables:U.K.

where:

(6)The mixing parameter and the logarithmic variation coefficient shall be the values  and

and  respectively for which the following amount becomes minimal:U.K.

respectively for which the following amount becomes minimal:U.K.

where:

For the determination of the minimal amount, no values for the mixing parameter less than zero or exceeding 1 shall be considered.

C. Reserve risk method 1 U.K.

Input data and method-specific data requirements U.K.

(1)The data for estimating the undertaking-specific standard deviation for non-life reserve risk or NSLT health reserve risk of segment s shall consist of the following:U.K.

(a)

the sum of the best estimate provision at the end of the financial year for claims that were outstanding in segment s at the beginning of the financial year and the payments made during the financial year for claims that were outstanding in segment s at the beginning of the financial year;

(b)

the best estimate of the provision for claims outstanding in segment s at the beginning of the financial year.

The amounts referred to in points (a) and (b) shall be available separately for different financial years.

(2)The following method-specific data requirements shall apply:U.K.

(a)

the data are representative for the reserve risk that the insurance or reinsurance undertaking is exposed to during the following twelve months

(b)

data are available for at least five consecutive financial years;

(c)

the data are adjusted for amounts recoverable from reinsurance contracts and special purpose vehicles which are consistent with the reinsurance contracts and special purpose vehicles that are in place to provide cover for the following twelve months;

(d)

the data include the expenses incurred in servicing the insurance and reinsurance obligations.

(e)

the data fit the following assumptions:

i.

the amount referred to paragraph 1(a) in that particular segment and financial year is linear proportional in the best estimate of the provision for claims outstanding in that particular segment and financial year;

ii.

the variance of the amount referred to paragraph 1(a) in a particular segment and financial year is quadratic in the provision for claims outstanding in a particular segment and financial year;

iii.

the amount referred to paragraph 1(a) follows a lognormal distribution;

iv.

maximum likelihood estimation is appropriate.

Method specification U.K.

(3)For the purpose of paragraphs 4-6, the following notation shall apply:U.K.

(a)

the financial years are denoted by consecutive numbers starting with 1 for the first financial year for which data are available;

(b)

T denotes the latest financial year for which data are available;

(c)

for all financial years, the amount referred to paragraph 1(a) in segment s in a particular financial year t is denoted by yt ;

(d)

for all financial years, the best estimate of the provision for claims outstanding in segment s in a particular financial year t are denoted by xt .

(4)The undertaking-specific standard deviation for non-life reserve risk or NSLT health reserve risk of segment s shall be equal to the following:U.K.

where:

(a)

c denotes the credibility factor set out in section G;

(e)

σ(prem,s) denotes the standard parameter that should be replaced by the undertaking-specific parameter.

(5)The standard deviation function shall be equal to the following function of two variables:U.K.

where:

(6)The mixing parameter and the logarithmic variation coefficient shall be the values  and

and  respectively for which the following amount becomes minimal:U.K.

respectively for which the following amount becomes minimal:U.K.

where:

For the determination of the minimal amount, no values for the mixing parameter less than zero or exceeding 1 shall be considered.

D. Reserve risk method 2 U.K.

Input data and method-specific data requirements U.K.

(1)The data for estimating the undertaking-specific standard deviation for deviation for non-life reserve risk or NSLT health reserve risk of segment s shall consist of cumulative payment amounts for insurance or reinsurance claims in segment s (cumulative claims amounts), separately for each accident year and development year of the payments.U.K.

(2)The following method-specific data requirements shall apply:U.K.

(a)

the data are representative for the reserve risk that the insurance or reinsurance undertaking is exposed to during the following twelve months;

(b)

data are available for at least five consecutive accident years;

(c)

in the first accident year, data are available for at least five consecutive development years;

(d)

in the first accident year the cumulative payment amount of the last development year for which data are available includes all the payments of the accident year except an immaterial amount;

(e)

the number of consecutive accident years for which data are available is not less than the number of consecutive development years in the first accident year for which data are available;

(f)

the cumulative claims amounts are adjusted for amounts recoverable from reinsurance contracts and special purpose vehicles which are consistent with the reinsurance contracts and special purpose vehicles that are in place to provide cover for the following twelve months;

(g)

the cumulative claims amounts shall include the expenses incurred in servicing the insurance or reinsurance obligations;

(h)

the data are consistent with the following assumptions about the stochastic nature of cumulative claims amounts:

i.

cumulative claims amounts for different accident years are mutually stochastically independent;

ii.

for all accident years the implied incremental claim amounts are stochastically independent;

iii.

for all accident years the expected value of the cumulative claims amount for a development year is proportional to the cumulative claims amount for the preceding development year;

iv.

for all accident years the variance of the cumulative claims amount for a development year is proportional to the cumulative claims amount for the preceding development year.

For the purposes of point (d), a payment amount shall be considered to be material where ignoring it in the calculation of the undertaking-specific parameter could influence the decision-making or the judgement of the users of that information, including the supervisory authorities

Method specification U.K.

(3)For the purpose of paragraphs 4 and 5, the following notation shall apply:U.K.

(a)

the accident years are denoted by consecutive numbers starting with 0 for the first accident year for which data are available;

(b)

I denotes the latest accident year for which data are available;

(c)

J denotes the latest development year in the first accident year for which data are available;

(d)

C(i,j) denotes the cumulative claims for accident year i and development year j.

(4)The undertaking-specific standard deviation for non-life reserve risk or NSLT health reserve risk of segment s shall be equal to the following:U.K.

where:

(a)

c denotes the credibility factor set out in section G;

(b)

MSEP denotes the mean squared error of prediction as specified in paragraph 5;

(c)

for all accident years and development years,

where for all development years

(d)

σ(res,s) denotes the standard parameter for non-life reserve risk or NSLT health reserve risk of segment s.

(5) [F1The mean squared error of prediction shall be equal to the following: U.K.

where:

E. Revision risk method U.K.

Input data and method-specific data requirements U.K.

(1)The data for estimating the undertaking-specific increase in the amount of annuity benefits shall consist of annual amounts of annuity benefits of annuity insurance obligations where the benefits payable could increase as a result of changes in the legal environment or in the state of health of the person insured (annuity benefits), separately for consecutive financial years and each beneficiary.U.K.

(2)The following method-specific data requirements shall apply:U.K.

(a)

the data are representative for the revision risk that the insurance or reinsurance undertaking is exposed to during the following twelve months;

(b)

data are available for at least five consecutive financial years;

(c)

the annuity benefits are gross, without deduction of the amounts recoverable from reinsurance contracts and special purpose vehicles;

(d)

the annuity benefits shall include the expenses incurred in servicing the annuity obligations;

(e)

the data are consistent with the following assumptions about the stochastic nature of increases in the amount of annuity benefits:

i.

the annual number of annuity increases follows a negative binomial distribution, including in the tail of the distribution;

ii.

the amount of an annuity increase follows a lognormal distribution, including in the tail of the distribution;

iii.

the annual number of annuity increases and the amounts of the annuity increase are mutually stochastically independent.

Method specification U.K.

(3)For the purpose of paragraphs 4-8, the following notation shall apply:U.K.

(a)

the financial years are denoted by consecutive numbers starting with 1 for the first financial year for which data are available;

(b)

T denotes the latest financial year for which data are available;

(c)

A(i,t) denotes the annuity benefits of beneficiary i in financial year t;

(4)The undertaking-specific increase in the amount of annuity benefits shall be equal to the following:U.K.

where:

(a)

c denotes the credibility factor set out in section G;

(c)

VaR 0,995(R) denotes the 99,5 % quantile of the distribution of annuity increases set out in paragraph 6;

(d)

S is equal to 3 % where the calculation is done for the purpose of the revision risk sub-module set out in Article 141 and equal to 4 % where the calculation is done for the purpose of the health revision risk sub-module set out in Article 158.

(5)The expected value of annuity increases shall be equal to the following:U.K.

where:

(6)The annuity increases shall be equal to the following:U.K.

where:

(a)

N denotes the annual number of annuity increases and follows a negative binominal distribution with an expected value that is equal to the estimated number of changes in annuity benefits set out in point (b) of paragraph 5 and with a standard deviation that is equal to the estimated standard deviation of the number of changes in annuity benefits set out in paragraph 7;

(b)

Xk denotes the amount of an annuity increase and follows a lognormal distribution with an expected value that is equal to the estimated average change in annuity benefits set out in point (a) of paragraph 5 and with a standard deviation that is equal to the estimated standard deviation of changes in annuity benefits set out in paragraph 8;

(c)

the annual number of annuity increases and the amounts of the annuity increase are mutually stochastically independent.

(7)The estimated standard deviation of the number of changes in annuity benefits shall be equal to the following:U.K.

where:

(8)The estimated standard deviation of changes in annuity benefits shall be equal to the following:U.K.

where:

[F2F1. Non-proportional reinsurance method 1] U.K.

Input data and method-specific data requirements U.K.

(1)The data for estimating the undertaking-specific adjustment factor for non-proportional reinsurance shall consist of the ultimate claim amounts of insurance and reinsurance claims that were reported to the insurance or reinsurance undertaking in segment s during the last financial years, separately for each insurance and reinsurance claim.U.K.

(2)The following method-specific data requirements shall apply:U.K.

(a)

the data are representative for the premium risk that the insurance or reinsurance undertaking is exposed to during the following twelve months;

(b)

the data do not indicate a higher premium risk than reflected in the standard deviation for premium risk used to calculate the Solvency Capital Requirement;

(c)

the ultimate claim amounts are estimated in the year the insurance and reinsurance claims were reported;

(d)

data are available for at least five reporting years;

(e)

where the recognisable excess of loss reinsurance contract applies to gross claims, the ultimate claim amounts are gross;

(f)

where the recognisable excess of loss reinsurance contract applies to claims after deduction of the recoverables from certain other reinsurance contracts and special purpose vehicles, the amounts receivable from those certain other reinsurance contracts and special purpose vehicles are deducted from the ultimate claim amounts;

(g)

the ultimate claim amounts shall not include expenses incurred in servicing the insurance and reinsurance obligations;

(h)

the data are consistent with the assumption that ultimate claim amounts follow a lognormal distribution, including in the tail of the distribution.

Method specification U.K.

(3)For the purpose of paragraphs 4-7, the following notation shall apply:U.K.

(a)

insurance and reinsurance claims for which data are available are denoted by consecutive numbers starting with 1;

(b)

n denotes the number of insurance and reinsurance claim for which data are available;

(c)

Yi denotes the ultimate claim amount of insurance or reinsurance claim i;

(d)

μ and ω denote the first and second moment, respectively, of the claim amount distribution, being equal to the following amounts:

(e)

b 1 denotes the amount of the retention of the recognisable excess of loss reinsurance contract referred to in Article 218(2);

(f)

[F1where the recognisable excess of loss reinsurance contract referred to in Article 218(2) provides compensation only up to a specified limit, b2 denotes the amount of that limit.]

(4)The undertaking-specific specific adjustment factor for non-proportional reinsurance shall be equal to the following:U.K.

where:

(a)

c denotes the credibility factor set out in section G;

(b)

NP′ denotes the estimated adjustment factor for non-proportional reinsurance set out in paragraph 5;

(c)

NP denotes the adjustment factor for non-proportional reinsurance set out in Article 117(2).

(5)The estimated adjustment factor for non-proportional reinsurance shall be equal to the following:U.K.

where the parameters μ 2, ω 1 and ω 2 are set out in paragraph 6.

(6)The parameters, μ 2, ω 1 and ω 2 shall be equal to the following:U.K.

where:

(7)Notwithstanding paragraph 5, where non-proportional reinsurance covers homogeneous risk-groups within a segment, the estimated adjustment factor for non-proportional reinsurance shall be equal to the following:U.K.

where:

(a)

V(prem,h) denotes the volume measure for premium risk of the homogeneous risk group h determined in accordance with paragraph 3 of Article 116;

(b)

NP′(h) denotes the estimated adjustment factor for non-proportional reinsurance of homogeneous risk group h determined in accordance with paragraph 5.

Textual Amendments

F2 Substituted by Commission Delegated Regulation (EU) 2019/981 of 8 March 2019 amending Delegated Regulation (EU) 2015/35 supplementing Directive 2009/138/EC of the European Parliament and of the Council on the taking-up and pursuit of the business of Insurance and Reinsurance (Solvency II) (Text with EEA relevance).

[F3F2. Non-proportional reinsurance method 2 U.K.

Input data and method-specific data requirements U.K.

(1)

The data for estimating the undertaking-specific adjustment factor for non-proportional reinsurance shall consist of the aggregated annual losses of insurance and reinsurance claims that were reported to the insurance or reinsurance undertaking in segment s during the last financial years.

(2)

The following method-specific data requirements shall apply:

(a)

the data are representative for the premium risk that the insurance or reinsurance undertaking is exposed to during the following 12 months;

(b)

the data do not indicate a higher premium risk than reflected in the standard deviation for premium risk used to calculate the Solvency Capital Requirement;

(c)

the aggregated annual losses are estimated in the year the insurance and reinsurance claims were reported;

(d)

data are available for at least five reporting years;

(e)

where the recognisable stop loss reinsurance contract applies to gross claims, the aggregated annual losses are gross;

(f)

where the recognisable stop loss reinsurance contract applies to claims after deduction of the recoverables from certain other reinsurance contracts and special purpose vehicles, the amounts receivable from those certain other reinsurance contracts and special purpose vehicles are deducted from the aggregated annual losses;

(g)

the aggregated annual losses shall not include expenses incurred in servicing the insurance and reinsurance obligations;

(h)

the data are consistent with the assumption that aggregated annual losses follow a lognormal distribution, including in the tail of the distribution.

Method specification U.K.

(1)

For the purpose of paragraphs 4-7, the following notation shall apply:

(a)

n denotes the number of financial years for which aggregated annual losses data is available;

(b)

Y i denotes the aggregated losses in financial year i ;

(c)

μ and ω denote the first and second moment, respectively, of the aggregated annual losses distribution, being equal to the following amounts:

(d)

b 1 denotes the amount of the retention of the recognisable stop loss reinsurance contract referred to in Article 218(2);

(e)

where the recognisable stop loss reinsurance contract referred to in Article 218(2) provides compensation only up to a specified limit, b 2 denotes the amount of that limit.

(2)

The undertaking-specific specific adjustment factor for non-proportional reinsurance shall be equal to the following:

NP USP = c · NP′ + (1 – c ) · NP

where:

(a)

c denotes the credibility factor set out in section G;

(b)

NP′ denotes the estimated adjustment factor for non-proportional reinsurance set out in paragraph 5;

(c)

NP denotes the adjustment factor for non-proportional reinsurance set out in Article 117(2).

(3)

The estimated adjustment factor for non-proportional reinsurance shall be equal to the following:

where the parameters μ 1 , μ 2 , ω 1 and ω 2 are set out in paragraph 6.

(4)

The parameters μ 1 , μ 2 , ω 1 and ω 2 shall be equal to the following:

where:

(5)

Notwithstanding paragraph 5, where non-proportional reinsurance covers homogeneous risk-groups within a segment, the estimated adjustment factor for non-proportional reinsurance shall be equal to the following:

where:

(a)

V ( prem,h ) denotes the volume measure for premium risk of the homogeneous risk group h determined in accordance with paragraph 3 of Article 116;

(b)

NP′ ( h ) denotes the estimated adjustment factor for non-proportional reinsurance of homogeneous risk group h determined in accordance with paragraph 5.]

Textual Amendments

F3Inserted by Commission Delegated Regulation (EU) 2019/981 of 8 March 2019 amending Delegated Regulation (EU) 2015/35 supplementing Directive 2009/138/EC of the European Parliament and of the Council on the taking-up and pursuit of the business of Insurance and Reinsurance (Solvency II) (Text with EEA relevance).

G. Credibility factor U.K.

(1)The credibility factor for segments 1, 5 and 6 set out in Annex II shall be equal to the following:U.K.

| Time lengths in years | Credibility factor c |

|---|---|

| 5 | 34 % |

| 6 | 43 % |

| 7 | 51 % |

| 8 | 59 % |

| 9 | 67 % |

| 10 | 74 % |

| 11 | 81 % |

| 12 | 87 % |

| 13 | 92 % |

| 14 | 96 % |

| 15 and larger | 100 % |

(2)The credibility factor for segments 2 to 4 and 7 to 12 set out in Annex II, for the segments set out Annex XIV and for the revision risk method shall be equal to the following:U.K.

| Time lengths in years | Credibility factor c |

|---|---|

| 5 | 34 % |

| 6 | 51 % |

| 7 | 67 % |

| 8 | 81 % |

| 9 | 92 % |

| 10 and larger | 100 % |

(3)The time length shall be equal to the following:U.K.

(a)

for the premium risk method, the number of accident years for which data are available;

(b)

for reserve risk method 1, the number of financial years for which data are available;

(c)

for reserve risk method 2, the number of accident years for which data are available;

(d)

for the revision risk method, the number of financial years for which data are available;

(e)

for the non-proportional reinsurance method, the number of reporting years for which data are available.

Options/Help

Print Options

PrintThe Whole Regulation

PrintThis Annex only

You have chosen to open The Whole Regulation

The Whole Regulation you have selected contains over 200 provisions and might take some time to download. You may also experience some issues with your browser, such as an alert box that a script is taking a long time to run.

Would you like to continue?

You have chosen to open The Whole Regulation as a PDF

The Whole Regulation you have selected contains over 200 provisions and might take some time to download.

Would you like to continue?

You have chosen to open the Whole Regulation

The Whole Regulation you have selected contains over 200 provisions and might take some time to download. You may also experience some issues with your browser, such as an alert box that a script is taking a long time to run.

Would you like to continue?

You have chosen to open the Whole Regulation without Annexes

The Whole Regulation without Annexes you have selected contains over 200 provisions and might take some time to download. You may also experience some issues with your browser, such as an alert box that a script is taking a long time to run.

Would you like to continue?

You have chosen to open Schedules only

The Schedules you have selected contains over 200 provisions and might take some time to download. You may also experience some issues with your browser, such as an alert box that a script is taking a long time to run.

Would you like to continue?

Legislation is available in different versions:

Latest Available (revised):The latest available updated version of the legislation incorporating changes made by subsequent legislation and applied by our editorial team. Changes we have not yet applied to the text, can be found in the ‘Changes to Legislation’ area.

Original (As adopted by EU): The original version of the legislation as it stood when it was first adopted in the EU. No changes have been applied to the text.

See additional information alongside the content

Geographical Extent: Indicates the geographical area that this provision applies to. For further information see ‘Frequently Asked Questions’.

Show Timeline of Changes: See how this legislation has or could change over time. Turning this feature on will show extra navigation options to go to these specific points in time. Return to the latest available version by using the controls above in the What Version box.

Opening Options

Different options to open legislation in order to view more content on screen at once

More Resources

Access essential accompanying documents and information for this legislation item from this tab. Dependent on the legislation item being viewed this may include:

- the original print PDF of the as adopted version that was used for the EU Official Journal

- lists of changes made by and/or affecting this legislation item

- all formats of all associated documents

- correction slips

- links to related legislation and further information resources

Timeline of Changes

This timeline shows the different versions taken from EUR-Lex before exit day and during the implementation period as well as any subsequent versions created after the implementation period as a result of changes made by UK legislation.

The dates for the EU versions are taken from the document dates on EUR-Lex and may not always coincide with when the changes came into force for the document.

For any versions created after the implementation period as a result of changes made by UK legislation the date will coincide with the earliest date on which the change (e.g an insertion, a repeal or a substitution) that was applied came into force. For further information see our guide to revised legislation on Understanding Legislation.

More Resources

Use this menu to access essential accompanying documents and information for this legislation item. Dependent on the legislation item being viewed this may include:

- the original print PDF of the as adopted version that was used for the print copy

- correction slips

Click 'View More' or select 'More Resources' tab for additional information including:

- lists of changes made by and/or affecting this legislation item

- confers power and blanket amendment details

- all formats of all associated documents

- links to related legislation and further information resources

All content is available under the Open Government Licence v3.0 except where otherwise stated. This site additionally contains content derived from EUR-Lex, reused under the terms of the Commission Decision 2011/833/EU on the reuse of documents from the EU institutions. For more information see the EUR-Lex public statement on re-use.

All content is available under the Open Government Licence v3.0 except where otherwise stated. This site additionally contains content derived from EUR-Lex, reused under the terms of the Commission Decision 2011/833/EU on the reuse of documents from the EU institutions. For more information see the EUR-Lex public statement on re-use.