National Heritage Act 1980

An Act to establish a National Heritage Memorial Fund for providing financial assistance for the acquisition, maintenance and preservation of land, buildings and objects of outstanding historic and other interest; to make new provision in relation to the arrangements for accepting property in satisfaction of capital transfer tax and estate duty; to provide for payments out of public funds in respect of the loss of or damage to objects loaned to or displayed in local museums and other institutions; and for purposes connected with those matters.

Part I The National Heritage Memorial Fund

1 Establishment of National Heritage Memorial Fund.

(1)

There shall be a fund known as the National Heritage Memorial Fund, to be a memorial to those who have died for the United Kingdom, established in succession to the National Land Fund, which shall be applicable for the purposes specified in this Part of this Act.

(2)

The Fund shall be vested in and administered by a body corporate known as the Trustees of the National Heritage Memorial Fund and consisting of a chairman and not more than F1fourteen other members appointed by the Prime Minister.

(3)

The persons appointed under this section shall include persons who have knowledge, experience or interests relevant to the purposes for which the Fund may be applied and who are connected by residence or otherwise with England, Wales, Scotland and Northern Ireland respectively.

F2(3A)

The Prime Minister shall consult the Scottish Ministers before appointing—

(a)

the chairman of the Trustees, and

(b)

any person under this section on the ground that he is connected by residence or otherwise with Scotland.

(4)

References in this Part of this Act to the Trustees are to the body constituted by subsection (2) above; and Schedule 1 to this Act shall have effect with respect to the Trustees and the discharge of their functions.

2 Payments into the Fund.

(1)

F5(1A)

The Trustees shall pay into the Fund any sums paid to them under section 24 of the National Lottery etc. Act 1993.

(2)

There shall also be paid into the Fund any other sums received by the Trustees in consequence of the discharge of their functions.

F63 Financial assistance towards property, etc.

(1)

The powers of the Trustees to give financial assistance under this section are exercisable in the case of things of any kind which are of scenic, historic, archaeological, aesthetic, architectural, engineering, artistic or scientific interest, including animals and plants which are of zoological or botanical interest.

(2)

The Trustees may, for the purpose of—

(a)

securing the preservation or enhancement of such things,

(b)

encouraging the study and understanding of them and the compilation and dissemination of information about them,

(c)

securing or improving access to them, or their display,

(d)

encouraging enjoyment of them, or

(e)

encouraging the maintenance and development of the skills required for their preservation or enhancement,

or for any purpose ancillary to those purposes, give financial assistance for any project which appears to them to be of public benefit.

(3)

The projects for which financial assistance may be given under this section for any of the purposes mentioned in subsection (2) above include (among others) projects for any person to whom the assistance is to be given to—

(a)

acquire property of any kind (including land),

(b)

construct or convert buildings,

(c)

carry out other works, or

(d)

provide education or training.

(4)

Before giving any financial assistance under this section for any project, the Trustees—

(a)

shall obtain any expert advice about the project they consider appropriate, and

(b)

must be satisfied that the project is of importance to the national heritage.

(5)

Financial assistance under this section shall be given by way of grant or loan out of the Fund, and in giving such assistance the Trustees may impose any conditions they think fit.

(6)

The conditions that may be imposed in giving such assistance may relate (among other things) to—

(a)

maintenance, repair, insurance and safe-keeping,

(b)

means of access or display,

(c)

disposal or lending, or

(d)

repayment of grant or loan.

(7)

In giving any financial assistance under this section for any project for the preservation or enhancement of anything, or determining the conditions on which such assistance is to be given, the Trustees shall bear in mind the desirability of public access to, or the public display of, the thing in question and of its enjoyment by the public.

(8)

The Secretary of State may, with the consent of the Treasury, apply sums received by him under this section as money provided by Parliament instead of paying them into the Consolidated Fund

F73A Financial assistance towards exhibitions, archives, etc.

(1)

The Trustees may give financial assistance for any project within subsection (2) below which appears to them—

(a)

to relate to an important aspect of the history, natural history or landscape of the United Kingdom, and

(b)

to be of public benefit.

(2)

The projects within this subsection are projects for any person to whom the assistance is to be given to—

(a)

set up and maintain a public exhibition,

(b)

compile and maintain an archive,

(c)

publish archive material, or

(d)

compile and publish a comprehensive work of reference (or publish a comprehensive work of reference that has previously been compiled),

or to do any ancillary thing.

(3)

In subsection (2) above, “archive” includes any collection of sound recordings, images or other information, however stored.

(4)

Before giving any financial assistance under this section for any project, the Trustees shall obtain any expert advice about the project they consider appropriate.

(5)

Subsections (5), (6) and (8) of section 3 above apply for the purposes of this section as they apply for the purposes of that.

(6)

In giving any financial assistance under this section for any project to compile or maintain an archive, or determining the conditions on which such assistance is to be given, the Trustees shall bear in mind the desirability of public access to the archive

4 Other expenditure out of the Fund.

(1)

Subject to the provisions of this section, the Trustees may apply the Fund for any purpose other than making grants or loans, being a purpose connected with the acquisition, maintenance or preservation of property falling within F8subsection (2) below, including its acquisition, maintenance or preservation by the Trustees.

F9(2)

The property referred to in subsection (1) above is—

(a)

any land, building or structure which in the opinion of the Trustees is of outstanding scenic, historic, archaeological, aesthetic, architectural, engineering or scientific interest;

(b)

any object which in their opinion is of outstanding historic, artistic or scientific interest;

(c)

any collection or group of objects, being a collection or group which taken as a whole is in their opinion of outstanding historic, artistic or scientific interest;

(d)

any land or object not falling within paragraph (a), (b) or (c) above the acquisition, maintenance or preservation of which is in their opinion desirable by reason of its connection with land or a building or structure falling within paragraph (a) above; or

(e)

any rights in or over land the acquisition of which is in their opinion desirable for the benefit of land or a building or structure falling within paragraph (a) or (d) above.

(2A)

The Trustees shall not apply the Fund for any purpose under subsection (1) above in respect of any property unless they are of the opinion, after obtaining any expert advice they consider appropriate, that the property (or, in the case of land or an object falling within paragraph (d) of subsection (2) above, the land, building or structure with which it is connected, or in the case of rights falling within paragraph (e) of that subsection, the land, building or structure for whose benefit they are acquired) is of importance to the national heritage.

(2B)

Notwithstanding that an object such as is mentioned in subsection (2)(b) above or a collection or group of objects such as is mentioned in subsection (2)(c) above is not of itself of importance to the national heritage, the Trustees may apply the Fund under subsection (1) above for any purpose connected with its acquisition if—

(a)

they are satisfied that after the acquisition it will form part of a collection or group of objects such as is mentioned in subsection (2)(c) above, and

(b)

after obtaining any expert advice they consider appropriate, they are of the opinion that that collection or group is of importance to the national heritage.

(2C)

Subsection (7) of section 3 above shall have effect in relation to the application of any sums out of the Fund under this section as it has in relation to the making of a grant or loan under that section.

(3)

The Trustees shall not retain any property acquired by them under this section except in such cases and for such period as F10the Secretary of State may allow.

5 Acceptance of gifts.

(1)

Subject to the provisions of this section, the Trustees may accept gifts of money or other property.

(2)

The Trustees shall not accept a gift unless it is either unconditional or on conditions which enable the subject of the gift (and any income or proceeds of sale arising from it) to be applied for a purpose for which the Fund may be applied under this Part of this Act and which enable the Trustees to comply with subsection (3) below and section 2(2) above.

(3)

The Trustees shall not retain any property (other than money) accepted by them by way of gift except in such cases and for such period as F11the Secretary of State may allow.

(4)

References in this section to gifts include references to bequests and devises.

6 Powers of investment.

(1)

Any sums in the Fund which are not immediately required for any other purpose may be invested by the Trustees in accordance with this section.

(2)

Sums directly or indirectly representing money paid into the Fund under section 2(1) F12or (1A) above may be invested in any manner approved by the Treasury; and the Trustees—

(a)

shall not invest any amount available for investment which represents such money except with the consent of the Treasury; and

(b)

shall, if the Treasury so require, invest any such amount specified by the Treasury in such manner as the Treasury may direct.

F13(3)

The trustees may invest any sums to which subsection (2) does not apply in any investments in which trustees may invest under general power of investment in section 3 of the Trustee Act 2000 (as restricted by sections 4 and 5 of that Act).

7 Annual reports and accounts.

(1)

(2)

It shall be the duty of the Trustees—

(a)

to keep proper accounts and proper records in relation to the accounts;

(b)

to prepare in respect of each financial year a statement of account in such form as F14the Secretary of State may with the approval of the Treasury direct; and

(c)

to send copies of the statement to F14the Secretary of State and the Comptroller and Auditor General before the end of the month of November next following the end of the financial year to which the statement relates.

(3)

The Comptroller and Auditor General shall examine, certify and report on each statement received by him in pursuance of this section and lay copies of it and of his report before Parliament.

Part II Property Accepted in Satisfaction of Tax

8 Payments by Ministers to Commissioners of Inland Revenue.

(1)

Where under paragraph 17 of Schedule 4 to the M1Finance Act 1975 F15or section 230 of the Capital Transfer Tax Act 1984 the Commissioners of Inland Revenue have accepted any property in satisfaction of any amount of capital transfer tax, F16the Secretary of State may pay to the Commissioners a sum equal to that amount.

(2)

Any sums paid to the Commissioners under this section shall be dealt with by them as if they were payments on account of capital transfer tax.

(3)

Subsections (1) and (2) above shall apply in relation to estate duty chargeable on a death occurring before the passing of the said Act of 1975 as they apply in relation to capital transfer tax; and for that purpose the reference in subsection (1) to paragraph 17 of Schedule 4 to that Act shall be construed as a reference to—

(a)

section 56 of the M2Finance (1909-1910) Act 1910;

(b)

section 30 of the M3Finance Act 1953 and section 1 of the M4Finance (Miscellaneous Provisions) Act (Northern Ireland) 1954; and

(c)

section 34(1) of the M5Finance Act 1956, section 46 of the M6Finance Act 1973, Article 10 of the M7Finance (Northern Ireland) Order 1972 and Article 5 of the M8Finance (Miscellaneous Provisions) (Northern Ireland) Order 1973.

(4)

References in this Part of this Act to property accepted in satisfaction of tax are to property accepted by the Commissioners under the provisions mentioned in this section.

9 Disposal of property accepted by Commissioners.

(1)

Any property accepted in satisfaction of tax shall be disposed of in such manner as F17the Secretary of State may direct.

(2)

Without prejudice to the generality of subsection (1) above, F17the Secretary of State may in particular direct that any such property shall, on such conditions as he may direct, be transferred to any institution or body falling within F18subsection (2A) below which is willing to accept it, to the National Art Collections Fund or the Friends of the National Libraries if they are willing to accept it, to the Secretary of State or to the Department of the Environment for Northern Ireland.

F19(2A)

The institutions or bodies referred to in subsection (2) above are—

(a)

any museum, art gallery, library or other similar institution having as its purpose or one of its purposes the preservation for the public benefit of a collection of historic, artistic or scientific interest;

(b)

any body having as its purpose or one of its purposes the provision, improvement or preservation of amenities enjoyed or to be enjoyed by the public or the acquisition of land to be used by the public; and

(c)

any body having nature conservation as its purpose or one of its purposes.

(3)

Where F17the Secretary of State has determined that any property accepted in satisfaction of tax is to be disposed of under this section to any such institution or body as is mentioned in subsection (2) above or to any other person who is willing to accept it, he may direct that the disposal shall be effected by means of a transfer direct to that institution or body or direct to that other person instead of being transferred to the Commissioners.

(4)

F17The Secretary of State may in any case direct that any property accepted in satisfaction of tax shall, instead of being transferred to the Commissioners, be transferred to a person nominated by F17the Secretary of State; and where property is so transferred the person to whom it is transferred shall, subject to any directions subsequently given under subsection (1) or (2) above, hold the property and manage it in accordance with such directions as may be given by F17the Secretary of State.

(5)

In exercising F17his powers under this section in respect of an object or collection or group of objects having a significant association with a particular place, F17the Secretary of State shall consider whether it is appropriate for the object, collection or group to be, or continue to be, kept in that place, and for that purpose F17the Secretary of State shall obtain such expert advice as appears to F17him to be appropriate.

(6)

F17The Secretary of State shall lay before Parliament as soon as may be after the end of each financial year a statement giving particulars of any disposal or transfer made in that year in pursuance of directions given under this section.

(7)

References in this section to the disposal or transfer of any property include references to leasing, sub-leasing or lending it for any period and on any terms.

F20(8)

The functions of the Ministers under this section in relation to the disposal or transfer of property in which there is a Scottish interest may be exercised separately.

(9)

For the purposes of subsection (8) a Scottish interest in the property exists where–

(a)

the property is located in Scotland;

(b)

the person liable to pay the tax has imposed a condition on his offer of the property in satisfaction of tax that it be displayed in Scotland or disposed of or transferred to a body or institution in Scotland; or

(c)

only a body or institution. in Scotland has expressed an interest in acquiring the property; or

(d)

a body or institution in Scotland and another body or institution have expressed an interest in acquiring the property.

10 Receipts and expenses in respect of property accepted by Commissioners.

(1)

(2)

Any sums received on the disposal of, or of any part of, the property (including any premium, rent or other consideration arising from the leasing, sub-leasing or lending of the property) and any sums otherwise received in connection with the property shall be paid to F21the Secretary of State.

(3)

Any expenses incurred in connection with the property so far as not disposed of under section 9 above, including in the case of leasehold property any rent payable in respect of it, shall be defrayed by F21the Secretary of State.

11 Exemption from stamp duty.

No stamp duty shall be payable on any conveyance or transfer of property made under section 9 above to any such institution or body as is mentioned in subsection (2) of that section or on any conveyance or transfer made under subsection (4) of that section.

F2211A.Stamp duty land tax

(1)

A land transaction—

(a)

which is entered into under section 9 above and by which property is transferred to any such institution or body mentioned in subsection (2) of that section, or

(b)

which is entered into under subsection (4) of that section,

is exempt from charge for the purposes of stamp duty land tax.

(2)

Relief under this section must be claimed in a land transaction return or an amendment of such a return.

(3)

In this section—

“land transaction” has the meaning given by section 43(1) of the Finance Act 2003;

“land transaction return” has the meaning given by section 76(1) of that Act.

12 Approval of property for acceptance in satisfaction of tax.

(1)

. . . F23

(2)

The power of the Commissioners of Inland Revenue to accept property in satisfaction of estate duty under the provisions mentioned in subsection (3) of section 8 above shall not be exercisable except with the agreement of F24the Secretary of State; and F24the Secretary of State shall exercise the functions conferred on the Treasury by the provisions mentioned in paragraphs (b) and (c) of that subsection. . . F25.

(3)

Any question whether an object or collection or group of objects is pre-eminent shall be determined under the provisions mentioned in section 8(3)(b) or (c) above in the same way as under F26section 230(4) of the Capital Transfer Tax Act 1984.

13 Acceptance of property in satisfaction of interest on tax.

(1)

. . . F27

(2)

References to estate duty in—

(a)

the provisions mentioned in section 8(3) above; and

(b)

section 32 of the M9Finance Act 1958 and section 5 of the M10Finance Act (Northern Ireland) 1958,

shall include references to interest payable under section 18 of the M11Finance Act 1896.

(3)

Section 8 above shall have effect where by virtue of this section F28or section 230(1) or 231(2) of the Capital Transfer Tax Act 1984 property is accepted in satisfaction of interest as it has effect where property is accepted in satisfaction of capital transfer tax or estate duty and references in this Part of this Act to property accepted in satisfaction of tax shall be construed accordingly.

14 Transfer of Ministerial functions.

(1)

(2)

An Order under this section may contain such incidental, consequential and supplemental provisions as may be necessary or expedient for the purpose of giving effect to the Order, including provisions adapting any of the provisions referred to in subsection (1) above.

(3)

No Order shall be made under this section unless a draft of the Order has been laid before, and approved by a resolution of, each House of Parliament.

F3115 Abolition of National Land Fund.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Part III Miscellaneous and Supplementary

16 Indemnities for objects on loan.

(1)

Subject to subsections (3) and (4) below, F32the Secretary of State may, in such cases and to such extent as he may determine, undertake to indemnify any institution, body or person F33. . . for the loss of, or damage to, any object belonging to that institution, body or person while on loan to any other institution, body or person F34which falls within subsection (2) below.

(2)

The institutions, bodies and persons F35which fall within this subsection are—

(a)

a museum, art gallery or other similar institution in the United Kingdom which has as its purpose or one of its purposes the preservation for the public benefit of a collection of historic, artistic or scientific interest and which is maintained—

(i)

wholly or mainly out of moneys provided by Parliament or out of moneys appropriated by Measure; or

(ii)

by a local authority or university in the United Kingdom;

(b)

a library which is maintained—

(i)

wholly or mainly out of moneys provided by Parliament or out of moneys appropriated by Measure: or

(ii)

by a library authority;

or the main function of which is to serve the needs of teaching and research at a university in the United Kingdom;

(c)

the National Trust for Places of Historic Interest or Natural Beauty;

(d)

the National Trust for Scotland for Places of Historic Interest or Natural Beauty; and

(e)

any other body or person for the time being approved for the purposes of this section by F32the Secretary of State with the consent of the Treasury.

(3)

F36The Secretary of State shall not give an undertaking under this section unless he considers that the loan will facilitate public access to the object in question or contribute materially to public understanding or appreciation of it.

(4)

F36The Secretary of State shall not give an undertaking under this section unless the loan of the object in question is made in accordance with conditions approved by him and the Treasury and F32the Secretary of State is satisfied that appropriate arrangements have been made for the safety of the object while it is on loan.

(5)

Subsections (1) to (4) above shall apply in relation to the loan of an object belonging to an institution, body or person established or resident in Northern Ireland with the substitution for references to F32the Secretary of State and the Treasury of references to the Department of Education for Northern Ireland and the Department of Finance for Northern Ireland respectively.

(6)

In subsection (2) above “library authority” means a library authority within the meaning of the M12Public Libraries and Museums Act 1964, a statutory library authority within the meaning of the M13Public Libraries (Scotland) Act 1955 or an Education and Library Board within the meaning of the M14Education and Libraries (Northern Ireland) Order 1972 and “university” includes a university college and a college, school or hall of a university.

(7)

References in this section to the loss of or damage to, or to the safety of, an object while on loan include references to the loss of or damage to, or the safety of, the object while being taken to or returned from the place where it is to be or has been kept while on loan.

F37(8)

The power of either of the Ministers to give an undertaking under this section regarding any object lost or damaged while on loan to an institution, body or person in Scotland may be exercised separately.

F3816A Reporting of indemnities given under section 16.

(1)

For each of the successive periods of six months ending with 31st March and 30th September in each year, F39the Secretary of State shall prepare a report specifying—

(a)

the number of undertakings given by him under section 16 above during that period; and

(b)

the amount or value, expressed in sterling, of any contingent liabilities as at the end of that period in respect of such of the undertakings given by him under that section at any time as remain outstanding at the end of that period.

(2)

A report under subsection (1) above shall be laid before Parliament not later than two months after the end of the period to which it relates.

(3)

Subsections (1) and (2) above shall apply in relation to undertakings given under section 16 above by the Department of Education for Northern Ireland—

(a)

with the substitution for references to F39the Secretary of State of references to that Department; and

(b)

with the substitution for the reference to Parliament in subsection (2) of a reference to the Northern Ireland Assembly.

F40(4)

The duties of each of the Ministers under subsections (1) and (2) in relation to undertakings given under section 16 above regarding any object lost or damaged while on loan to an institution, body or person in Scotland may be exercised separately.

17 Expenses and receipts.

18 Short title, interpretation, repeals and extent.

(1)

This Act may be cited as the National Heritage Act 1980.

(2)

In this Act—

“financial year” means the twelve months ending with 31st March;

. . . F43

. . . F44

(3)

. . . F45

(4)

References in this Act to the making of a grant or loan or the transfer or conveyance of any property to any institution or body include references to the making of a grant or loan or the transfer or conveyance of property to trustees for that institution or body.

(5)

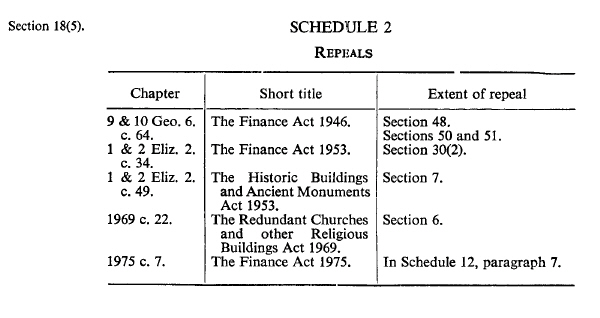

The enactments mentioned in Schedule 2 to this Act are hereby repealed to the extent specified in the third column of that Schedule.

(6)

This Act extends to Northern Ireland.

SCHEDULE 1 The Trustees of the National Heritage Memorial Fund

Status

1

The Trustees shall not be regarded as acting on behalf of the Crown and neither they nor their officers or servants shall be regarded as Crown servants.

2

F46Section 40 of the M15General Rate Act 1967 (relief for charities and other organisations)F46F47Sections 43(6), F4845(6)F4845A and 47 of F47Section 47 of, and paragraph 2 of Schedule 4ZA, paragraph 2 of Schedule 4ZB and paragraph 2 of Schedule 5A to, the Local Government Finance Act 1988, section 4 of the M16Local Government (Financial Provisions etc.) (Scotland) Act 1962 (corresponding provisions for Scotland) and Article 41 of the M17Rates (Northern Ireland) Order 1977 (corresponding provisions for Northern Ireland) shall apply to any hereditament, lands and heritages occupied by the Trustees for the purposes of this Act as they apply to a hereditament, lands and heritages occupied by trustees for a charity.

Tenure of office of trustee

3

(1)

Subject to the provisions of this paragraph, a member of the body constituted by section 1(2) of this Act (in this Schedule referred to as “a trustee”) shall hold and vacate his office in accordance with the terms of his appointment.

(2)

A person shall not be appointed a trustee for more than three years.

(3)

A trustee may resign by notice in writing to the Prime Minister.

(4)

The Prime Minister may terminate the appointment of a trustee if he is satisfied that—

(a)

for a period of six months beginning not more than nine months previously he has, without the consent of the other trustees, failed to attend the meetings of the trustees;

(b)

he is an undischarged bankrupt or has made an arrangement with his creditors or is insolvent within the meaning of paragraph 9(2)(a) of Schedule 3 to the M18Conveyancing and Feudal Reform (Scotland) Act 1970;

F49(ba)

he is a person in relation to whom a moratorium period under a debt relief order applies (under Part 7A of the Insolvency Act 1986);

(c)

he is by reason of physical or mental illness, or for any other reason, incapable of carrying out his duties; or

(d)

he has been convicted of such a criminal offence, or his conduct has been such, that it is not in the Prime Minister’s opinion fitting that he should remain a trustee.

F50(4A)

The Prime Minister shall consult the Scottish Ministers before exercising any power of his under sub-paragraph (4)(d) above to terminate the appointment of a trustee in respect of whose appointment he was required by section 1(3A) of this Act to consult those Ministers.

(5)

A person who ceases or has ceased to be a trustee may be re-appointed.

Tenure of office of chairman

4

(1)

Subject to the provisions of this paragraph, the chairman of the Trustees shall hold and vacate his office in accordance with the terms of his appointment.

(2)

The chairman may resign his office by notice in writing to the Prime Minister.

(3)

A trustee who ceases or has ceased to be chairmen may be reappointed to that office.

(4)

If the chairman ceases to be a trustee he shall also cease to be chairman.

F51Remuneration

F524A

There may be paid out of the Fund to a trustee such remuneration, on such terms and conditions, as the Secretary of State may approve.

Expenses and allowances

5

(1)

All administrative and other expenses incurred by the Trustees in discharging their functions F53may be defrayed out of the Fund.

(2)

There may be paid out of the Fund to a trustee such allowances as F54the Trustees think fit.

Staff

F556

The Trustees may appoint such officers and servants as they think fit, on such terms (including terms as to remuneration and pensions) as they think fit.

Proceedings

7

(1)

Subject to the provisions of this Act—

(a)

the Trustees shall discharge their functions in accordance with such arrangements as they may determine; and

(b)

those arrangements may provide for any function to be discharged under the general direction of the Trustees by a committee or committees consisting of three or more trustees.

(2)

Anything done by a committee under the arrangements shall, if the arrangements so provide, have effect as if done by the Trustees.

(3)

The validity of any proceedings of the Trustees shall not be affected by any vacancy among the trustees or by any defect in the appointment of a trustee.

(4)

The arrangements made under this paragraph may include provisions specifying a quorum for meetings of the Trustees and any committee; and until a quorum is so specified in relation to meetings of the Trustees the quorum for such meetings shall be such as may be determined by F56the Secretary of State.