Finance Act 1966

An Act to grant certain duties, to alter other duties, and to amend the law relating to the National Debt and the Public Revenue, and to make further provision in connection with Finance.

Part I Customs and Excise

1. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F1

F22 Reliefs for shipbuilders in respect of certain duties.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F3

4, 5.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F4

6. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F5

7. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F6

8. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F7

9. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F8

10, 11.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F9

Duties relating to betting and gaming

12 General Betting Duty.

(1)—(5)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F10

(6)

The pool betting duty shall not be chargeable on any bet made as mentioned in subsection (1)(c) of this section on or after 24th October 1966, and accordingly from that date—

(a)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F10

(b)

paragraph 4(a)(i) of Schedule 5 to the M1Betting, Gaming and Lotteries Act 1963 (which relates to the disposal of amounts staked by means of a totalisator on a dog racecourse) for the words “pool betting duty” there shall be substituted the words “general betting duty” ;

and as from that date bookmakers’ licence duty shall cease to be charged.

13. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F11

14. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F12

Duties relating to betting and gaming

15 Additional or supplementary provisions as to duties on betting or gaming.

(1)—(4)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F13

(5)

The supplemental provisions set out in Schedule 3 to this Act shall have effect with respect to the duties relating to betting and gaming.

(6)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F13

16. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F14

Part II

17—25.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F15

Part III CORPORATION TAX ACTS

26. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F16

F1727 Amendments of Corporation Tax Acts.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

28. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F18

29. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F19

30. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F20

31, 32.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F21

33, 34.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F22

Part IV

35—39.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F23

40. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F24

Part V

41, 42.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F25

43. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F26

Part VI

44. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F27

Part VII Miscellaneous

F2845 Harbour reorganisation schemes: corporation tax and stamp duty.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

46. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F29

47. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F30

48. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F31

49—51.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F32

52. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F33

53 Short title, construction, extent and repeals.

(1)

This Act may be cited as the Finance Act 1966.

(2)

In this Act Part I shall be construed as one with the F34M2Customs and Excise Management Act 1979; . . . F35; Part III shall be construed as one with the Corporation Tax Acts; . . . F35; . . . F36; and so much of Part VII as relates to stamp duties shall be construed as one with the M3Stamp Act 1891.

(3)

Any reference in this Act to any other enactment shall, except so far as the context otherwise requires, be construed as a reference to that enactment as amended or applied by or under any other enactment, including this Act.

(4)

Except as otherwise expressly provided, such of the provisions of this Act as relate to matters in respect of which the Parliament of Northern Ireland has power to make laws shall not extend to Northern Ireland.

(5)

This Act, in so far as it affects the operation of the Sugar Act 1956, shall extend to the Isle of Man.

(6)

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F37

(7)

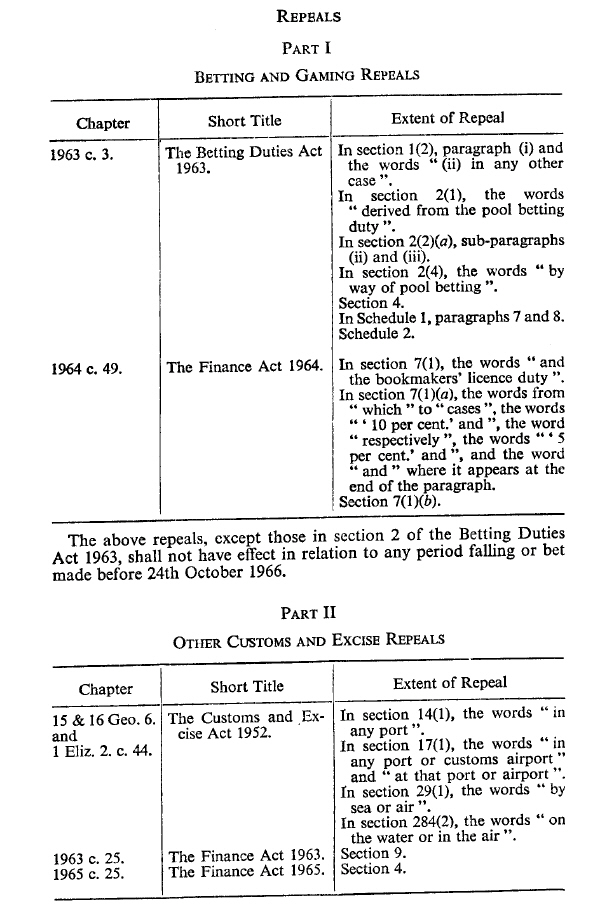

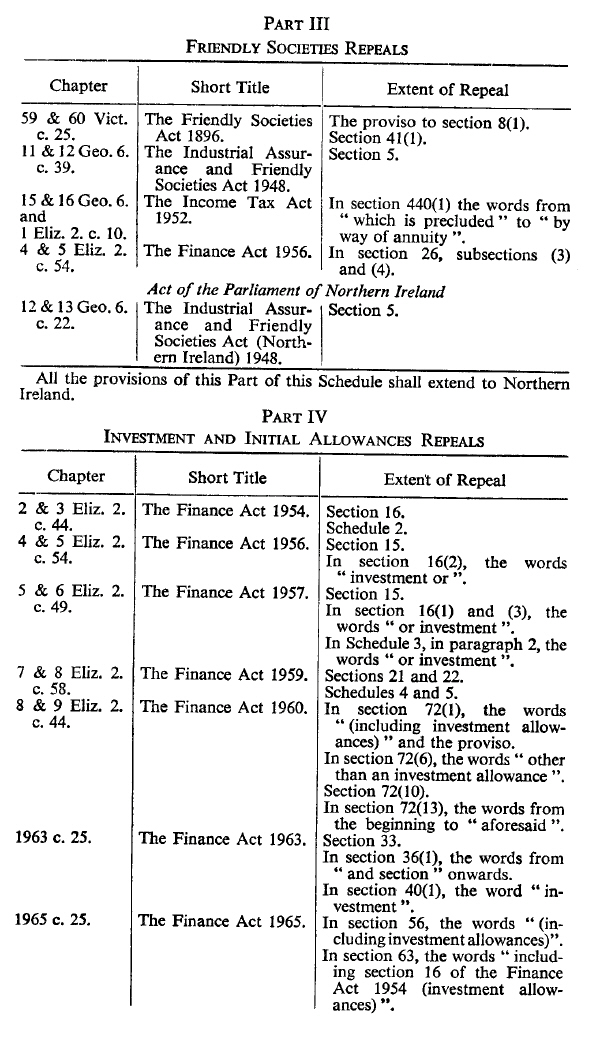

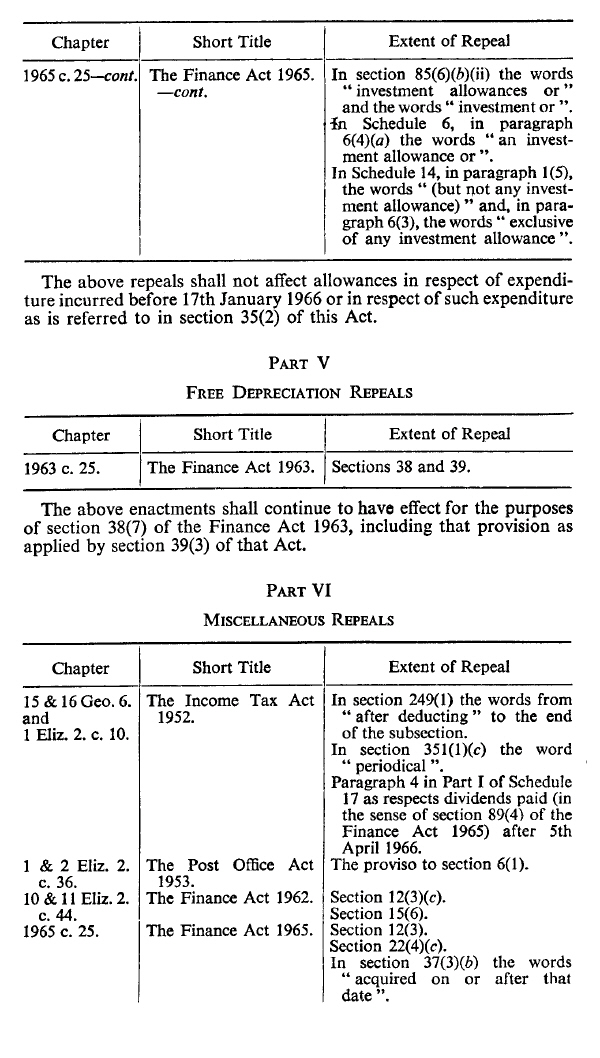

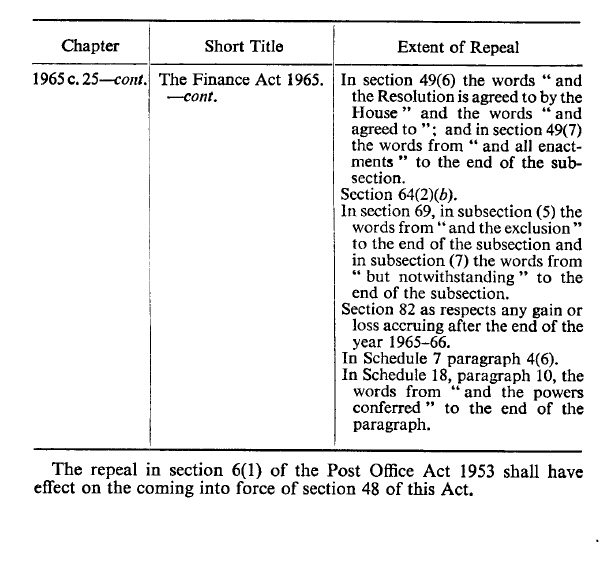

The enactments mentioned in Schedule 13 to this Act are hereby repealed to the extent mentioned in the third column of that Schedule, but subject to any provision in relation thereto made at the end of any Part of that Schedule.

SCHEDULE 1 Reliefs For Shipbuilders

Part I Determination of Open Market Value

1

(1)

The open market value of any vessel or other structure and its fittings and equipment shall be taken for the purposes of section 2 of this Act to be the price which they would fetch at the time of their delivery pursuant to the contract in question on a sale in the open market between buyer and seller independent of each other.

(2)

The said price shall be determined on the assumption that the buyer will bear freight, insurance and all other costs, charges and expenses incurred in respect of the vessel or structure and other items in question after their delivery as aforesaid or, where delivery is to be effected outside the United Kingdom, after their departure from the United Kingdom for the purpose.

(3)

For the purposes of this paragraph, a sale in the open market between a buyer and seller independent of each other presupposes—

(a)

that the vessel or structure and other items in question are the sole consideration for the price paid, and

(b)

that the price is not influenced by any commercial, financial or other relationship, whether by contract or otherwise, between the seller or any person associated in business with him and the buyer or any person associated in business with him (other than the relationship created by the sale of the said vessel or structure and other items), and

(c)

that neither the seller nor any person associated in business with him has provided any part of the price, and that no part of the price will be returned to the buyer or any person associated in business with him.

(4)

For the purposes of the last foregoing sub-paragraph, two persons shall be deemed to be associated in business with one another if, whether directly or indirectly, either of them has any interest in the business or property of the other, or both have a common interest in any business or property, or some third person has an interest in the business or property of both of them.

Part II Reductions in Purchase Price or Open Market Value

2

(1)

Where the amount payable in respect of any vessel or other structure under the said section 2 is, by virtue of subsection (3) thereof, to be determined by reference to the price payable as mentioned in that subsection, then—

(a)

if the terms of the contract in question are such that the applicant for the payment will bear any of the following, that is, any freight, insurance or other costs, charges or expenses incurred in respect of the vessel or structure or its fittings or equipment after their delivery pursuant thereto or, where delivery is to be effected outside the United Kingdom, after their departure from the United Kingdom for the purpose, the price shall be treated for the purposes of that subsection as reduced by an amount reflecting the burden thus assumed by the applicant;

(b)

if the whole or any part of the price is payable twelve months or more after the time when the property in the vessel or structure passes or, if later, the time of delivery of the vessel or structure or of its departure from the United Kingdom for the purpose of delivery, the price shall be treated for those purposes as reduced by an amount representing the discount which would be chargeable for obtaining payment at that earlier time at a rate of interest equal to the bank rate then prevailing.

(2)

In the foregoing sub-paragraph “bank rate” means the minimum rate at which the Bank of England will lend to a discount house having access to the Discount Office of the Bank.

3

If, after consultation with the Board of Trade, it appears to the Commissioners that the fittings and other equipment supplied with any vessel or other structure include any items the supply of which would not in the ordinary course of events be undertaken by a person building such a vessel or structure for delivery to another as that other’s property, the price or, as the case may be, open market value referred to in the said subsection (3) shall be treated for the purposes of that subsection as reduced by an amount equal to the open market value of the items in question; and the provisions of paragraph 1 of this Schedule shall apply for the purpose of determining that value, subject to any necessary modifications.

Part III Supplemental

4

The following provisions of the F38M4Customs and Excise Management Act 1979 shall apply in relation to payments under the said section 2 as they apply in relation to drawbacks, allowances or repayments under F38the Customs and Excise Acts 1979, that is to say, F38section 135 (time limit on payment), F38section 136(1) and (2) (offences in connection with claims) and F38section 167(4) (recovery of overpayments).

5

(1)

Any officer or person authorised by the Commissioners may require any person who has been concerned at any stage with a vessel or other structure in respect of which an application has been made under the said section 2, or with any fittings or other equipment supplied therewith, or with any payment in respect of the vessel or structure or any fittings or other equipment so supplied—

(a)

to furnish, within such time as that officer or person may require, such information as may be reasonably necessary to enable the Commissioners to determine whether the applicant is entitled to a payment under that section, or liable to make any repayment thereunder, or to determine the amount of any payment to which the applicant is so entitled, and

(b)

to produce for inspection by that officer or person, at such time and place as he may require, any books or accounts or other document of whatever nature relating to, or to any payment in respect of, the said vessel, structure, fittings or equipment.

(2)

Any such officer or person shall be entitled to take extracts from or make copies of any document produced to him under the foregoing sub-paragraph.

(3)

If any person fails to comply with any requirement under sub-paragraph (1) above, he shall be liable to a penalty of F39level 3 on the standard scale, together with a further penalty of ten pounds for each day during which failure to comply with the requirement continues.

6

(1)

Any dispute as to the determination for the purposes of an application under the said section 2 of the price or value referred to in subsection (3) of that section, or of any amount by which that price or value is to be treated as reduced by virtue of subsection (4) thereof, shall be referred to a referee appointed in accordance with the next following sub-paragraph.

(2)

A reference under the foregoing sub-paragraph shall be to a person (not being an official of any government department) appointed by the Lord Chancellor F40with the concurrence of the Lord Chief Justice of England and Wales or, if the application for the purposes of which the determination is made relates to a vessel or structure constructed in Scotland or Northern Ireland, or was by a company incorporated in Scotland or Northern Ireland, and the applicant in either case so requires, appointed by the Lord President of the Court of Session or as the case may be, F41by the Lord Chancellor with the concurrence of the Lord Chief Justice of Northern Ireland.

(3)

The procedure on any such reference shall be such as the referee may determine.

(4)

Sub-paragraph (1) above shall not have effect, and any price, value or amount falling to be determined for the purposes of the said subsection (3) or (4) shall be that fixed by the Commissioners, unless, within three months from the time when the Commissioners’ final determination thereof is communicated to him, or such longer time as the Commissioners may allow, a notice requiring a reference under that sub-paragraph has been served on the Commissioners by the person for the purposes of whose application the determination was made.

F42(5)

The Lord Chief Justice of England and Wales may nominate a judicial office holder (as defined in section 109(4) of the Constitutional Reform Act 2005) to exercise his functions under this paragraph.

(6)

The Lord Chief Justice of Northern Ireland may nominate any of the following to exercise his functions under sub-paragraph (2)—

(a)

the holder of one of the offices listed in Schedule 1 to the Justice (Northern Ireland) Act 2002;

(b)

a Lord Justice of Appeal (as defined in section 88 of that Act).

7

The making by the Commissioners of a payment under the said section 2 determined by reference to the price or value referred to in subsection (3) of that section, or that price or value as reduced by virtue of subsection (4) thereof, shall not be taken as constituting the making by the Commissioners of a final decision under the said subsection (3).

SCHEDULE 2.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F43

SCHEDULE 3 Supplementary Provisions as to Duties relating to Betting and Gaming

Part I Duties relating to Betting

1—5.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F44

F456

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7—26.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F46

SCHEDULE 4.. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F47

SCHEDULE 5 Amendments of Corporation Tax Acts

1—18.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F48

Transitional relief for company with overseas trading income which is a member of a group

F4919

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F50

F51SCHEDULE 6 Administration of Corporation Tax Acts

F511—13.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F51 Priority of corporation tax and other tax in liquidation

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

F51 Transitional relief for existing companies with overseas trading income

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .