Commission Decision (EU) 2018/859

of 4 October 2017

on State aid SA.38944 (2014/C) (ex 2014/NN) implemented by Luxembourg to Amazon

(notified under document C(2017) 6740)

(Only the French text is authentic)

(Text with EEA relevance)

THE EUROPEAN COMMISSION,

Having regard to the Treaty on the Functioning of the European Union, and in particular the first subparagraph of Article 108(2) thereof,

Having regard to the Agreement on the European Economic Area, and in particular Article 62(1)(a) thereof,

Whereas:

By letter of 21 November 2014, Luxembourg submitted its comments to the Opening Decision. That submission included, inter alia, a transfer pricing report prepared by [Advisor 2] on behalf of Amazon (‘the TP Report’), which had not been previously submitted to the Commission.

By letter of 13 February 2015, the Commission sent an additional request for information to Luxembourg. In that letter, the Commission also asked Luxembourg to agree that it could contact Amazon directly to obtain the requested information if that information was not in Luxembourg's possession. On 24 February 2015, Luxembourg requested an extension of deadline to reply to the Commission's request for information.

By letter of 5 March 2015, Amazon submitted its observations on the Opening Decision. Comments on the Opening Decision were also submitted by the following third parties: Oxfam on 14 January 2015, the Bundesarbeitskammer on 4 February 2015, Fedil on 27 February 2015, the Booksellers Association (‘BA’) on 3 March 2015, le Syndicat de la librairie française (‘SLF’) on 4 March 2015, the European and International Booksellers Federation (‘EIBF’) on 4 March 2015, ATOZ S.A. on 5 March 2015, the Computer and Communications Industry Association (‘CCIA’) on 5 March 2015 and the European Policy Information Center (‘EPICENTER’) on 5 March 2015. In addition, the Federation of European Publishers (‘FEP’) on 5 March 2015 and le Syndicat des Distributeurs de Loisirs Culturels (‘SDLC’) on 5 March 2015 expressed their support of the EIBF's position.

On 12 March 2015, a telephone conference took place between the Commission and Luxembourg in which the latter assured the former that it would be able to provide a complete reply to the Commission's request for information of 13 February 2015 by 17 March 2015.

By letter of 17 March 2015, Luxembourg partially replied to the Commission's request for information of 13 February 2015. It further explained that outstanding information, in particular that concerning certain contractual relationships between Amazon entities in Luxembourg and third parties, was not in its possession.

On 19 March 2015, the Commission transmitted the comments of third parties on the Opening Decision to Luxembourg.

By email exchanges of 18, 19 and 20 March 2015, the Commission indicated to Luxembourg that its reply of 17 March 2015 to the Commission's request for information of 13 February 2015 was incomplete and it posed further questions for clarification.

By letter of 20 April 2015, Luxembourg requested the Commission to explain the purpose of a meeting the latter had held with Oxfam and Eurodad, of which Luxembourg had not been informed. It also submitted a request not to publish the decision to send the MIT request.

On 4 May 2015, Amazon partially replied to the Commission's request for information of 26 March 2015. Amazon also confirmed that its structure in Luxembourg had changed in 2014 and that a new ruling was granted by Luxembourg on that basis, but explained that the change was irrelevant for the purposes of the Commission's investigation.

On 8 May 2015, a meeting was held between the Commission, Luxembourg and Amazon. By letter of 12 June 2015, Amazon submitted further comments following that meeting. Amazon also submitted a list of IP agreements, referred to by Amazon as the ‘M.com Agreements’, pursuant to which Amazon made IP related to its platform technology available to unrelated third parties.

By letter of 13 May 2015, Luxembourg submitted its observations on the third party comments on the Opening Decision.

By letter of 3 July 2015, the Commission reminded Amazon to provide certain outstanding information, in particular on the IP agreements, and asked for additional information.

By letter of 10 July 2015 (again submitted on 23 July 2015), Luxembourg submitted a statement concerning the non-retroactive application of a final negative decision of the Commission.

By letter of 31 July 2015, the Commission reminded Amazon to provide all requested information, in particular complete information on all IP agreements concluded by Amazon since 2000. It also requested Amazon to provide the new ruling granted to it by Luxembourg in 2014, to which a reference was made in Luxembourg's letter of 4 August 2014 and Amazon's letter of 4 May 2015.

By letter of 21 August 2015, Amazon replied to the Commission's request, except for the submission of information on the remaining IP agreements.

On 8 September 2015, a meeting took place between the Commission and Amazon of which Luxembourg was informed. Following that meeting, the Commission reminded Amazon by email of 8 September 2015 about the outstanding request for information concerning the IP agreements.

By email of 14 September 2015, Amazon explained that no other agreements exist pursuant to which the same intellectual property as that covered the License Agreement was or will be made available to related or unrelated parties. At the same time, Amazon informed the Commission that it was preparing a list of intra-group IP agreements, regardless of whether they relate to the EU or intellectual property covered by the License Agreement between LuxSCS and LuxOpCo. That list was submitted to the Commission on 17 September 2015.

By email of 23 September 2015, Amazon submitted a list of agreements by means of which intellectual property was licensed in from or licensed out to third parties.

By email of 29 September 2015, the Commission reminded Amazon to submit the IP agreements as requested by the Commission on 26 March and 3 July 2015 on the basis of the lists provided by Amazon on 17 and 23 September 2015. In addition, the Commission requested further information from Amazon concerning the cost sharing reports and LuxOpCo's customers per website.

By e-mails of 30 September and 1, 2, 12, 13, 20 and 27 October 2015, Amazon submitted information.

On 28 October 2015, a meeting took place between the Commission, Luxembourg and Amazon.

By email of 20 November 2015, the Commission reminded Amazon about the scope of its request for information of 26 March 2015 regarding Amazon's internal and external IP agreements and requested Amazon to submit additional information.

During a meeting on 27 November 2015, a company which requested its name not to be revealed (‘Company X’) provided the Commission with market information in relation to the Commission's investigation. In a conference call on 15 January 2016, Company X provided additional information on the e-commerce business in Europe. By email of 25 January 2016 regarding the minutes of the conference call, Company X provided additional information.

On 30 November 2016, Amazon submitted additional information.

By email of 1 December 2015, Amazon requested an extension to reply to the Commission's request for information dated 20 November 2015.

On 4 December 2015, Amazon submitted the information requested by the Commission in its email of 20 November 2015 and asked for an extension of deadline for the remaining responses.

By letters of 10 and 28 December 2015, Luxembourg submitted its observations following the meeting of 28 October 2015.

By email of 11 December 2015, the Commission reminded Amazon about the outstanding replies from its information request of 20 November 2015 and sent a further request for information with additional questions to Amazon.

On 18 December 2015, Amazon provided further responses to the Commission's request for information of 20 November 2015.

By email of 18 December 2015, the Commission invited Luxembourg to submit its observations and comments on the information submitted by Amazon to the Commission by that point of the investigation.

On 12 and 15 January 2016, Amazon submitted partial responses to the Commission's information request of 11 December 2015 and asked for an extension of deadline for the outstanding information.

On 18 January 2016, Amazon submitted further information.

By email of 19 January 2016, the Commission informed Amazon that certain replies to questions of previous requests for information were still outstanding. In addition, the Commission requested clarification and further information.

On 22 January 2016, Amazon partially replied to the Commission's request for information of 19 December 2015. On 28 January 2016, Amazon submitted a partial reply to the Commission's request for information of 11 December 2015. By letters of 5, 15, 19 and 24 February 2016, Amazon submitted partial replies to the Commission's request for information of 19 January 2016.

On 26 February 2016, the Commission sent a reminder to Amazon requesting it to reply to outstanding questions concerning the requests for information of 20 November 2015, 11 and 18 December 2015 and 19 January 2016.

On 4 and 21 March 2016, Amazon submitted partial replies to the Commission's request for information of 11 December 2015.

By email of 11 March 2016, Amazon submitted a partial reply to the Commission's request for information of 26 February 2016.

By email of 22 March 2016, Amazon submitted a partial reply to the Commission's requests for information of 19 January 2016 and 26 February 2016.

By email of 8 March 2016, Amazon agreed to waive confidentiality claims previously made vis-à-vis Luxembourg in a letter of 22 January 2016 for certain information submitted and committed to share this information with Luxembourg.

On 14 March 2016, Amazon confirmed to have shared its latest submission to the Commission with Luxembourg.

On 1 April 2016, the Commission requested Company X to agree that certain market information provided by it would be shared with Luxembourg. On 5 April 2016, Company X provided its agreement.

On 8 April 2016, the Commission inquired with Amazon about the information that Amazon had shared with Luxembourg by that point of the investigation. The Commission also informed Amazon that certain information of the Commission's request for information of 11 February 2015 was still outstanding. In addition, the Commission addressed a request for further clarification and information to Amazon.

By email of 11 April 2016, Amazon confirmed what information it had shared with Luxembourg.

By letter of 18 April 2016, the Commission inquired with Luxembourg what information had been shared with it by Amazon and invited Luxembourg to submit its comments on those submissions. The Commission further recalled its email of 18 December 2015, by which it had invited Luxembourg to comment on Amazon's submissions. Finally, the Commission shared the market information as agreed with Company X with Luxembourg and asked Luxembourg for its comments.

On 22 April 2016, Amazon submitted a partial reply to the Commission's request for information of 8 April 2016 and requested an extension of the deadline for the remaining replies.

By letter of 2 May 2016 (again submitted on 10 May 2016), Luxembourg confirmed receipt of the information submitted by Amazon by that point of the investigation and submitted its observations on Amazon's submissions. As regards the market information of Company X, Luxembourg informed the Commission that it had shared that information with Amazon, since Amazon would be in a better position to comment.

By email of 2 May 2016, Amazon submitted a partial reply and acknowledged the outstanding replies to questions raised in the Commission's request for information dated 8 April 2016, as mentioned in the letter of 22 April 2016.

By email of 17 May 2016, the Commission clarified the scope of the information it previously requested from Amazon and recalled that certain information was still outstanding from its requests for information of 11 December 2015 and 8 April 2016.

By email of 24 May 2016, Amazon submitted its reply to the Commission's email of 17 May 2016.

On 26 May 2016, a meeting between the Commission, Luxembourg and Amazon took place. During that meeting and in the draft minutes thereof, the Commission raised further questions to Amazon. By letter of 20 June 2016, Amazon replied to those questions.

By letter of 21 June 2016, Amazon submitted its comments to the market information of Company X. It also requested access to the complete submission of Company X and the disclosure of its identity.

On 7 July 2016, the Commission provided its comments to the amended minutes of the meeting of 26 May 2016 to Amazon. In addition, the Commission requested further information from Amazon.

By email of 22 July 2016, Amazon submitted a partial reply to the Commission's request for information of 7 July 2016. In its reply, Amazon informed the Commission about the protective order covering documents used in US Tax Court proceedings. Therefore, Amazon suggested submitting redacted documents, since these were available to Amazon.

By email of 27 July 2016, the Commission reminded Amazon about outstanding information following its request for information of 7 July 2016 and accepted to receive temporarily documents from the US Tax Court proceedings in a redacted version. In addition, the Commission requested further clarification and information from Amazon.

By email of 29 July 2016, Amazon submitted a partial reply to the Commission's request for information of 7 July 2016 and requested an extension of the deadline to reply to the remaining questions. By letter of 12 August 2016, Amazon submitted a partial reply to the Commission's request for information of 7 July 2016 and 27 July 2016.

By email of 19 August 2016, the Commission requested further clarification and information from Amazon concerning Amazon's replies to the request for information of 7 July 2016.

By email of 19 August 2016, and again by letter of 22 August 2016, the Commission sent a request for information to Amazon asking for the entire redacted documents of the US Tax Court proceedings.

On 26 August 2016, Amazon submitted a partial reply to the Commission's request for information of 7 July 2016 and requested an extension of the deadline to complete its reply.

By email of 30 August 2016, Amazon informed the Commission about its successful application concerning access to the documents used in the US Tax Court proceedings and announced the upcoming submission of unredacted documents.

On 9 September 2016, Amazon submitted a partial reply to the Commission's request for information dated 19 August 2016.

On 30 September 2016, Amazon submitted the unredacted documents as produced in the US Tax Court proceedings, as requested by the Commission on 22 August 2016.

By e-mails of 7 and 19 December 2016, the Commission asked Amazon for additional information concerning the US Tax Court proceedings. On 20 December 2016, Amazon submitted its reply.

On 21 December 2016, the Commission sent a request for information to Amazon to which Amazon submitted a partial reply on 20 January 2017. By email of 2 February 2017, the Commission sent Amazon further clarifications concerning its request for information of 21 December 2017. On 6, 8 and 27 February and 6 March 2017, Amazon submitted further information and partial replies to the Commission. By email of 13 March 2017, the Commission reminded Amazon to submit outstanding information.

On 14 March 2017, the Commission sent a request for information to Amazon.

By email of 24 March 2017, Amazon submitted the opinion of the US Tax Court of 23 March 2017 to the Commission.

By email of 27 March 2017, the Commission requested further information from Amazon concerning the US Tax Court's opinion.

On 28 March 2017, Amazon replied to the Commission requesting more time to answer due to the ongoing post-trial procedures in the US.

By email of 4 April 2017, Amazon submitted a partial reply to the Commission's request for information of 14 March 2017.

By email of 7 April 2017, the Commission informed Luxembourg and Amazon that it was obliged to decline Amazon's request to grant full access to the submissions of Company X.

On 11 April 2017, Amazon submitted another partial reply to the Commission's request for information of 14 March 2017 and requested an extension of the deadline for some remaining parts of its reply.

By email of 12 April 2017, Amazon submitted a partial reply to the Commission.

On 17 April 2017, Amazon submitted further information concerning the post-trial procedure in the US.

On 18 May 2017, Amazon sent another partial reply and thus completed its reply to the Commission's request for information of 14 March 2017.

By email of 19 May 2017, the Commission sent a request for information to Amazon.

On 29 May 2017, Amazon submitted further information to the Commission.

By email of 7 June 2017, Amazon submitted its reply to the Commission's request for information of 19 May 2017.

By email of 14 June 2017, the Commission requested Amazon to confirm that all information submitted by Amazon to the Commission in 2016 and 2017 had also been shared with Luxembourg and invited Luxembourg to submit its observations on the information submitted to the Commission by Amazon at that point of the investigation. On 19 June 2017, Amazon confirmed to have shared all information submitted to the Commission in 2016 and 2017 with Luxembourg. By email of 21 June 2017, Luxembourg confirmed to have received all documents that were submitted to the Commission by Amazon in 2016 and 2017 and that Luxembourg had no further comments in relation to Amazon's submissions to the Commission in 2016 and 2017 except for Amazon's submissions of 30 September 2016 and 20 January 2017.

On 22 June 2017, a meeting was held between the Commission, Luxembourg and Amazon.

On 6 July 2017, Luxembourg submitted its comments to submissions made by Amazon on 30 September 2016 and 20 January 2017.

On 6 July 2017, the Commission sent a request for information to Amazon to which Amazon replied on 10 and 27 July, and 4 and 7 August 2017.

By email of 9 August 2017, the Commission sent a request for information to Amazon. On 7 September 2017, Amazon submitted its reply.

On 12 September 2017, Luxembourg confirmed by email that it had no further comments to Amazon's submissions of 10 and 27 July, 4 and 7 August and 7 September 2017.

The Amazon group consists of Amazon.com, Inc. and all companies directly or indirectly controlled by Amazon.com, Inc. (collectively referred to as ‘Amazon’ or the ‘Amazon group’). Amazon is headquartered in Seattle, Washington, United States of America.

Amazon operates retail and service businesses.

Finally, Amazon manufactures and sells hardware products, such as Amazon Kindle, Amazon Fire and Amazon Echo devices.

The North America segment's sales primarily consist of retail sales of consumer products (including by third-party sellers) and subscriptions through North America-focused websites such as www.amazon.com, www.amazon.ca, and www.amazon.com.mx. That segment also includes export sales from those websites.

The International segment's sales primarily consist of retail sales of consumer products (including by third-party sellers) and subscriptions through international websites such as www.amazon.com.au, www.amazon.com.br, www.amazon.cn, www.amazon.in, www.amazon.co.jp, the EU websites and www.amazon.nl. That segment also includes export sales from these international websites (including export sales from these sites to customers in the U.S., Mexico, and Canada), but excludes export sales from Amazon's North American websites.

The AWS segment consists of global sales of computer, storage, database, and other service offerings for start-ups, enterprises, government agencies, and academic institutions. Through AWS, Amazon provides access to technology infrastructure for different types of business.

‘After having made myself acquainted with the letter of october [sic] 31, 2003, directed to me by [Advisor 1] just as with your letter of octobre [sic] 23, 2003 and dealing with your position regarding Luxembourg tax treatment within the framework of your future activities, I am pleased to inform you that I may approve the contents of the two letters.’

In its letter of 31 October 2003 to the Luxembourg tax administration (‘Amazon's letter of 31 October 2003’), Amazon sought confirmation of the tax treatment of LuxSCS, its US-based partners and dividends received by LuxOpCo under that structure. That letter explains that LuxSCS, as a Société en Commandite Simple, is not deemed to have a separate tax personality from that of its partners and, as a result, it is not subject to corporate income tax or net wealth tax in Luxembourg.

That letter refers to an ‘economic analysis’ attached thereto, which sets out ‘the functions and risks that LuxOpCo was anticipated to undertake, as well as the nature and extent of the Intangibles that are anticipated to be the subject of the Intangibles License’ concluded between LuxSCS and LuxOpCo. On the basis of that analysis, a transfer pricing arrangement was proposed under which the level of the annual royalty (referred to in the letter as the ‘License Fee’) that LuxOpCo would be required to pay to LuxSCS for the use of the Intangibles was established.

- ‘1.

Compute and allocate to LuxOpCo the ‘LuxOpCo Return’, which is equal to the lesser of (a) [4-6] % of LuxOpCo's total EU Operating Expenses for the year and (b) total EU Operating Profit attributable to the European Web Sites for such year;

- 2.

The License Fee shall be equal to EU Operating Profit minus the LuxOpCo Return, provided that the License Fee shall not be less than zero;

- 3.

The Royalty Rate for the year shall be equal to the License Fee divided by total EU Revenue for the year;

- 4.

Notwithstanding the foregoing, the amount of the LuxOpCo Return for any year shall not be less than 0,45 % of EU Revenue, nor greater than 0,55 % of EU Revenue;

- 5.

- (a)

In the event that the LuxOpCo Return determined under step (1) would be less than 0,45 % of EU Revenues, the LuxOpCo Return shall be adjusted to equal the lesser of (i) 0,45 % of Revenue or EU Operating Profit or (ii) EU Operating Profit;

- 6.

- (b)

In the event that the LuxOpCo Return determined under step (1) would be greater than 0,55 % of EU Revenues, the LuxOpCo Return shall be adjusted to equal the lesser of (i) 0,55 % of EU Revenues or (ii) EU Operating Profit.’

‘EU COGS’ means Costs of Goods Sold, computed using US GAAP (Generally Accepted Accounting Principles), attributable to LuxOpCo's operation of the European Web Sites.

‘EU Operating Expense’ means LuxOpCo's total costs, including intercompany expenses, but excluding: EU COGS, the License Fee, currency gains and losses and interest expense, calculated under U.S. GAAP.

‘EU Revenues’ means total net sales revenue earned by LuxOpCo through the EU Web Sites, which shall be equal to the sum of (a) the total sales prices of products sold by LuxOpCo, stated on the invoices which are issued to customers, including revenue attributable to gift wrapping and shipping and handling, less: value added taxes, returns and other allowances, and (b) total services revenue earned by LuxOpCo in connection with the sale of products or services by unrelated parties through the EU Web Sites, less value added taxes.

‘EU Operating Profit’ means EU Revenue minus: EU COGS and EU Operating Expenses.

Section 3 of the TP Report provides a functional analysis of LuxSCS and LuxOpCo.

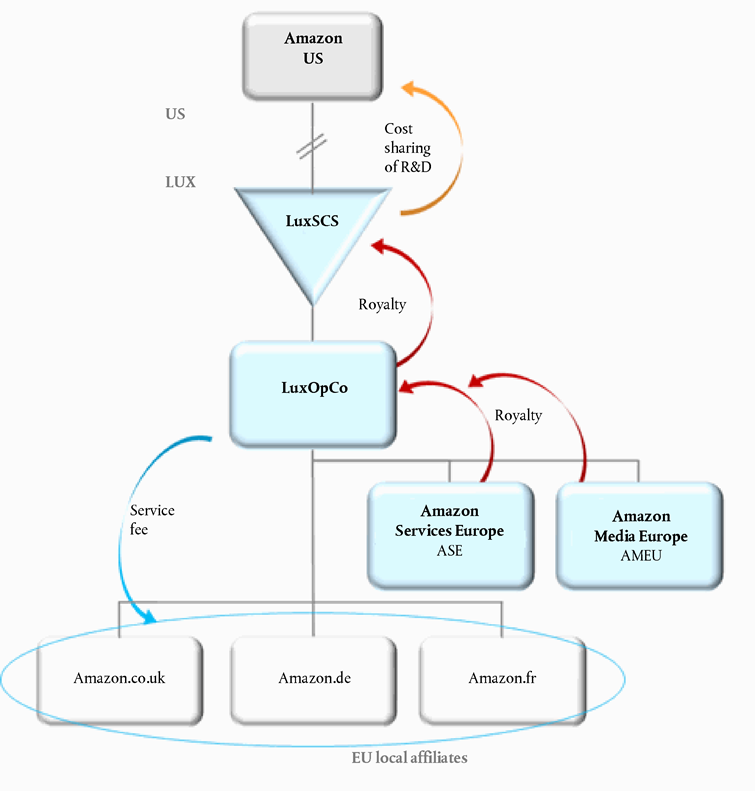

LuxOpCo was to contract with ASE, which would act as a service commission agent in its own name but for the benefit of LuxOpCo, in connection with Amazon's third-party seller programs in Europe. ASE's services would primarily consist of certain order processing services associated with the service business.

Section 5 of the TP Report deals with the selection of the most appropriate transfer pricing method for determining the arm's length nature of the Royalty Rate.

Section 6.1 of the TP Report calculates an arm's length range for royalty on the basis of the CUP method.

First of all, searches were performed for comparable transactions in Amazon's own internal database of license agreements and an external agency was commissioned to conduct a search for license agreements involving intangible assets similar to those of Amazon. The transactions identified as a result of the searches were not considered sufficiently comparable and were therefore rejected for the purpose of the CUP analysis.

To make that compensation comparable to the License Fee (referred to in the TP Report as the ‘Royalty Rate’), the set-up fees were amortized and allocated to each of the four periods referred to in the agreement and, together with the annual basic fee, they were converted into a percentage of sales (ranging from 3,4 % to 7,2 %). Since the commission fee included in the [A] Agreement ranged from 4 % to 5 % of sales, the TP Report's first conclusion was that the implied royalty rate in the [A] Agreement ranged from 8,4 % to 11,7 % of sales. However, [A] had also committed to pay Amazon certain fees to compensate for both excess order capacity and excess inventory level. Those fees, referred to in the agreement, were also converted into a percentage of sales, ranging from 1,2 % to 0,7 %. Therefore, the arm's length range for the Royalty Rate was initially calculated to be between 9,6 % and 12,6 % of sales.

Finally, since the [A] Agreement did not provide [A] with access to Amazon's customer data, the TP Report included an adjustment to align the CUP with the fact that LuxSCS granted LuxOpCo access to Amazon's customer data. Accordingly, using the information available in the [B] Agreement, an upward adjustment of 1 % was proposed, resulting in an arm's length range for the Royalty Rate between 10,6 % and 13,6 % of LuxOpCo's sales.

(EUR million) | ||||||||

1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|

2005 | 2006 | 2007 | 2008 | 2009 | 2010 | |||

a | Revenue | 3 154,2 | 4 299,9 | 5 073,9 | 5 987,1 | 7 064,7 | 8 336,3 | |

b | COGS | 2 446,9 | 3 332,7 | 3 932,6 | 4 640,5 | 5 475,8 | 6 461,4 | |

c | Gross Profit | a – b | 707,3 | 967,2 | 1 141,3 | 1 346,6 | 1 588,9 | 1 874,9 |

d | Operating expense | 89,9 | 106,0 | 121,7 | 143,7 | 171,2 | 204,2 | |

e | Intercompany (co.uk, .de, .fr) | 279,4 | 338,4 | 395,6 | 456,2 | 524,1 | 602,7 | |

f | LUX Commissionaire expense | 2,8 | 3,4 | 4,1 | 4,9 | 5,9 | 7,0 | |

g | Operating expense (incl. Intercompany) | d + e + f | 372,1 | 447,8 | 521,4 | 604,8 | 701,2 | 813,9 |

h | Estimated Operating Net Profit (Loss) before Routine Return | c – g | 335,2 | 519,4 | 619,9 | 741,8 | 887,7 | 1 061,0 |

i | Routine Return to LuxASE | 0,14 | 0,17 | 0,20 | 0,24 | 0,29 | 0,35 | |

j | Routine Return to LuxOpCo | [4 – 6] % × g | 16,8 | 20,2 | 23,5 | 27,2 | 31,6 | 36,6 |

k | Estimated Residual Profit Payable to LuxSCS | h – i – j | 318,3 | 499,1 | 596,2 | 714,3 | 855,8 | 1 024,0 |

l | Effective Royalty Rate (as % of Revenue) | k/a | 10,1 % | 11,6 % | 11,8 % | 11,9 % | 12,1 % | 12,3 % |

Summarising the transfer pricing analyses of the License Agreement using the CUP method and the residual profit split method, the TP Report considered that the results converge and indicated that an arm's length range for the Royalty Rate from LuxOpCo to LuxSCS under that agreement is 10,1 % to 12,3 % of LuxOpCo's sales.

(EUR million) | ||||||||

Luxembourgish fiscal unity group | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|---|

Total revenue | 1 979,4 | 3 545,7 | 4 298,6 | 5 605,4 | 7 628,8 | 10 086,3 | 13 312,1 | [15 000 – 15 500] |

Net COGS | 1 610,8 | 2 828,3 | 3 406,1 | 4 421,6 | 6 084,4 | 8 078,0 | 10 486,6 | [11 500 – 12 000] |

Total operating expense | 262,5 | 476,8 | 530,0 | 637,6 | 918,3 | 1 461,7 | 2 252,9 | [3 000 – 3 500] |

Thereof | ||||||||

Expenses applicable to mark-up | 262,5 | 439,9 | 493,6 | 597,0 | 801,9 | 1 313,1 | 2 041,7 | [2 500 – 3 000] |

Thereof | ||||||||

LuxOpCo - OpEx | 78,6 | 162,6 | 203,6 | 258,4 | 317,7 | 483,1 | 662,7 | [800 – 900] |

LuxOpCo - Intercompany | 183,8 | 277,3 | 290,0 | 338,6 | 484,1 | 830,1 | 1 379,0 | [1 500 – 2 000] |

Expenses excluded from mark-up (Mngt and RSU) | 0,0 | 36,9 | 36,4 | 40,6 | 116,4 | 148,5 | 211,2 | [200 – 300] |

Resulting operating profit | 106,1 | 240,5 | 362,6 | 546,2 | 626,1 | 546,6 | 572,7 | [600 – 700] |

Estimated Total Return to Lux Fiscal Unity Group at [4-6] % of adjusted OpEx | 11,8 | 19,8 | 22,2 | 26,9 | 36,1 | 59,1 | 91,9 | [100 – 200] |

Ceiling/floor analysis | ||||||||

Profit ceiling (0,55 % of revenue) | 10,9 | 19,5 | 23,6 | 30,8 | 42,0 | 55,5 | 73,2 | [80 – 90] |

Profit floor (0,45 % of revenue) | 8,9 | 16,0 | 19,3 | 25,2 | 34,3 | 45,4 | 59,9 | [60 – 70] |

Luxembourg consolidated Profit - per Ceiling/Floor and Return | 10,9 | 19,5 | 22,2 | 26,9 | 36,1 | 55,5 | 73,2 | [80 – 90] |

Royalty payment (Lux fiscal unity group to LuxSCS) | 95,2 | 221,0 | 340,4 | 519,3 | 590,0 | 491,1 | 499,4 | [500 – 600] |

The application of the [4-6] % mark-up on the sum of LuxOpCo's operating expenses and intercompany expenses produces the Estimated Total Return To Lux Fiscal Unity Group. This result is then tested against the ceiling and the floor criteria (0,55 % and 0,45 % of revenues respectively). In cases where the Estimated Total Return was higher than 0,55 % of the revenues (as in years 2006, 2007, 2011, 2012 and 2013), the application of the ceiling was determinant for assessing LuxOpCo's taxable income in Luxembourg, referred to in Table 2 as the ‘Luxembourg consolidated Profit – per Ceiling/Floor and Return’.

Finally, the Luxembourg consolidated Profit (referred to as the LuxOpCo return in the ruling request) is subtracted from the operating profit (referred to as the ‘EU Operating profit’ in the ruling request) to determine the License Fee due to LuxSCS.

During the course of the investigation, Amazon provided information on the European online retail market, on its business model in general and on its European operations in particular, on the IP licensing agreements it concluded with unrelated entities, and on its new corporate and tax structure in Luxembourg with effect from June 2014. That information complements the information already presented in Sections 2.1 and 2.2.

- (a)

Software platform: the software code developed by Amazon to operate its web sites consists of complex software tools that run the various features of the websites, such as search and navigation, order processing and personalisation. The software tools at the root of the platform form an integrated system that is constantly being improved, reinforced and modified. The main features include operating speed, extent of functions and flexibility in the response to users' needs.

- (b)

Appearance of the website: the design creates a unique ‘presentation’ of the website.

- (c)

Catalogue software: the catalogue consists of all the information on the products sold by Amazon on its websites. Amazon's catalogue is notable for the extent of the information on products that it can obtain through querying other services, such as availability and pricing data.

- (d)

Search and navigation function software: the software tools supporting the search and navigation functions of the websites allow the large quantity of information contained in the product catalogues to be flexibly and logically organised and sorted. The site navigation developers use these tools to organise the data so that they can maximise the likelihood that customers will find what they are looking for.

- (e)

Logistics software: the logistics process uses software developed by Amazon to manage the inventory, supply chain, logistics and restocking.

- (f)

Order processing software: order processing uses software developed by Amazon to perform certain functions, in particular communication with Amazon order management centres to confirm product availability, validate dispatch, estimate the delivery date, and communicate gift packaging requirements and other customer preferences.

- (g)

Customer service software: the customer service representatives use software developed by Amazon to monitor customer orders and respond fully and quickly to the wide variety of these.

- (h)

Personalisation functions software: Amazon has developed, and is continuing to develop software tools that enable the Amazon databases to store, organise and retrieve a large amount of data on the preferences and purchase history of individual customers. This function results in a better experience for users and is more likely to generate repeat purchases.

In its submissions of 18 December 2015 and 15 January 2016, Amazon presented an overview of the organisational structure of LuxOpCo as of the end of 2013, describing the departments of the company.

[…]

(EUR million) | ||||||||

LuxOpCo profit and loss | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|---|

Turnover | n.a. | n.a. | n.a. | n.a. | n.a. | 9 130,1 | 11 892,9 | [13 500 – 14 000] |

COGS | n.a. | n.a. | n.a. | n.a. | n.a. | 7 078,4 | 9 171,9 | [10 000 – 10 500] |

Net turnover | 1 930,1 | 3 426,7 | 4 031,6 | 5 191,1 | 7 042,1 | 2 051,7 | 2 721,0 | [3 000 – 3 500] |

Staff costs | 2,2 | 5,1 | 7,5 | 11,4 | 14,0 | 23,4 | 40,7 | [60 – 70] |

Value adjustments on assets | 4,0 | 14,9 | 16,1 | 15,9 | 31,8 | 81,8 | 254,4 | [200 – 300] |

Other operating income | 91,3 | 128,6 | 211,7 | 286,6 | 451,0 | 724,6 | 1 183,1 | [1 500 – 2 000] |

Thereof | ||||||||

Royalty received from ASE | 78,6 | 126,1 | 196,2 | 285,6 | 449,8 | 694,3 | 1 072,3 | [1 500 – 2 000] |

Royalty received from AMEU | 2,5 | 7,5 | 0,0 | 0,0 | 21,9 | 95,9 | [100 – 200] | |

Other operating (external) charges | 1 979,5 | 3 546,8 | 4 188,5 | 5 416,5 | 7 418,2 | 2 647,3 | 3 726,2 | [4 500 – 5 000] |

Thereof | ||||||||

COGS | 2 608,4 | 3 058,4 | 3 952,6 | 5 458,1 | ||||

Royalty paid to LuxSCS | 95,2 | 257,9 | 341,4 | 519,3 | 590,0 | 491,1 | 499,4 | [500 – 600] |

Interest receivable and similar income | 10,9 | 22,7 | 29,7 | 19,2 | 23,8 | 65,4 | 131,1 | [40 – 50] |

Interest payable and similar charges | 30,4 | 16,5 | 35,5 | 38,3 | 33,1 | 60,5 | 80,0 | [70-80] |

(19,5) | 6,2 | (5,7) | (19,1) | (9,3) | 4,9 | 51,1 | [30 – 40] | |

Tax on profit and similar charges | 4,6 | (1,6) | 6,7 | 4,2 | 5,5 | 8,2 | 2,2 | [0 – 10] |

Profit (loss) for the financial year | 11,6 | (3,7) | 18,8 | 10,6 | 14,4 | 20,4 | (68,3) | [20 – 30] |

LuxOpCo balance sheet | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|---|

Assets | ||||||||

Fixed assets | 190 | 209 | 275 | 304 | 547 | 915 | 1 361 | [1 500 – 2 000] |

Intangible fixed assets | 0 | 0 | 0 | 0 | 0 | 2 | 121 | [100 – 200] |

Tangible fixed assets | 6 | 5 | 1 | 1 | 3 | 5 | 8 | [0-10] |

Financial fixed assets | 184 | 203 | 274 | 303 | 544 | 908 | 1 232 | [1 500-2 000] |

Current assets | 887 | 1 171 | 1 518 | 2 396 | 3 255 | 4 113 | 4 851 | [5 000-5 500] |

Inventories | 185 | 227 | 245 | 384 | 591 | 990 | 1 350 | [1 500-2 000] |

Debtors | 152 | 255 | 266 | 320 | 511 | 798 | 916 | [1 000 – 1 500] |

Transferable securities | 99 | 112 | 376 | 1 049 | 1 348 | 1 182 | 924 | [800-900] |

Cash at bank, cash in postal cheque account, cheques and cash in hand | 451 | 577 | 632 | 644 | 805 | 1 143 | 1 661 | [1 500-2 000] |

Prepayments | 0 | 0 | 1 | 1 | 5 | 3 | 16 | [10-20] |

Total assets | 1 077 | 1 380 | 1 794 | 2 702 | 3 807 | 5 031 | 6 228 | [7 000 – 7 500] |

Liabilities | ||||||||

Capital and reserves | 35 | 41 | 73 | 89 | 117 | 185 | 109 | [100 – 200] |

Non-subordinated debt | 1 011 | 1 302 | 1 676 | 2 521 | 3 553 | 4 636 | 5 817 | [6 500 – 7 000] |

Trade creditors | 397 | 597 | 779 | 1 136 | 1 661 | 2 187 | 2 910 | [3 000 – 3 500] |

Amounts owed to affiliated companies | 550 | 632 | 833 | 1 285 | 1 712 | 2 109 | 2 460 | [2 500-3 000] |

Tax and social security debts | 2 | 6 | 5 | 3 | 1 | 116 | 121 | [100-200] |

Other creditors and accruals | 61 | 68 | 59 | 96 | 179 | 224 | 327 | [100-200] |

Deferred income | 31 | 37 | 46 | 92 | 137 | 210 | 301 | [300-400] |

Total liabilities | 1 077 | 1 380 | 1 794 | 2 702 | 3 807 | 5 031 | 6 228 | [7 000-7 500] |

(EUR thousand) | |||||||||

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |

|---|---|---|---|---|---|---|---|---|---|

Value adjustments in respect of the current assets | n.a. | 8 043 | 12 556 | 15 343 | 170 176 | 54 908 | 80 858 | [70 000 – 80 000] | [40 000 – 50 000] |

Thereof: | |||||||||

Inventories | 12 694 | 45 664 | 68 251 | [60 000 – 70 000] | |||||

Trade debtors | 4 382 | 9 244 | 12 607 | [10 000 – 20 000] | |||||

Provisions for value adjustments: | |||||||||

For inventory | 16 525 | 19 340 | 25 127 | 35 482 | 48 320 | 91 060 | 152 543 | [200 000 – 300 000] | [200 000 – 300 000] |

Trade debtors – doubtful accounts | 6 022 | 11 019 | 13 739 | 9 019 | 11 739 | 1 653 | 16 042 | [10 000 – 20 000] | [20 000 – 30 000] |

(EUR million) | ||||||||

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |

|---|---|---|---|---|---|---|---|---|

Net sales proceeds | 1 798,9 | 3 152,7 | 3 849,4 | 5 019,6 | 6 751,5 | 8 741,0 | 11 166,3 | [12 000 – 12 500] |

Marketplace | 71,0 | 158,1 | 216,2 | 302,5 | 467,0 | 721,9 | 1 105,8 | [1 500 – 2 000] |

Digital | 0,0 | 23,2 | 28,7 | 26,6 | 58,9 | 146,2 | 369,5 | [500-600] |

Fulfillment by Amazon | 0,0 | 0,1 | 0,4 | 4,2 | 53,6 | 80,5 | 175,6 | [400-500] |

Prime subscription | 0,0 | 0,4 | 5,8 | 25,8 | 60,4 | 77,3 | 113,2 | [100-200] |

Transportation costs recharge | 74,8 | 135,1 | 125,9 | 124,9 | 117,8 | 160,2 | 208,9 | [100 – 200] |

Gift packaging | 2,9 | 4,4 | 4,6 | 5,4 | 11,7 | 14,6 | 24,4 | [20-30] |

Ancilliary revenues | 30,1 | 71,7 | 67,6 | 96,4 | 107,9 | 144,5 | 148,5 | [100-200] |

1 977,7 | 3 545,7 | 4 298,7 | 5 605,4 | 7 628,8 | 10 086,3 | 13 312,1 | [15 000 – 15 500] | |

(EUR million) | ||||||||

LuxOpCo external operating charges | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|---|

Building costs | 1,2 | 2,4 | 4,3 | 3,6 | 3,9 | 8,0 | 8,9 | [10-20] |

COGS | 1 486,6 | 2 608,4 | 3 058,4 | 3 952,6 | 5 458,1 | 0,0 | 0,0 | [20-30] |

Consulting, legal and other | 1,5 | 4,3 | 5,6 | 4,9 | 8,8 | 16,2 | 21,2 | [30 - 40] |

Employee | 2,5 | 2,4 | 3,2 | 3,3 | 4,7 | 11,7 | 25,2 | [20-30] |

Fulfillment | 3,1 | 6,0 | 8,1 | 10,1 | 15,2 | 25,2 | 42,9 | [60-70] |

Intercompany | 267,2 | 544,3 | 665,3 | 870,6 | 1 127,4 | 976,3 | 1 591,3 | [2 000-2 500] |

Marketing | 47,3 | 63,7 | 85,6 | 123,9 | 155,0 | 259,5 | 386,6 | [400-500] |

Others | 0,6 | – 0,3 | 11,3 | 2,0 | – 7,4 | – 4,6 | – 6,6 | – [0 – 10] |

Receivables and Credit Card fees | 24,7 | 46,0 | 47,5 | 49,0 | 60,4 | 57,6 | 55,9 | [60-70] |

Royalty | 0,0 | 0,3 | 2,0 | 29,9 | 66,1 | 0,0 | 0,5 | [0-10] |

Transportation | 145,0 | 269,2 | 297,2 | 366,6 | 525,9 | 794,3 | 1 065,9 | [1 000-1 500] |

Total | 1 979,5 | 3 546,8 | 4 188,5 | 5 416,5 | 7 418,2 | 2 144,1 | 3 191,8 | [4 000 – 4 500] |

(EUR million) | ||||||||

LuxOpCo marketing costs | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|---|

Ad placement | 0,0 | 0,9 | – 0,1 | 0,0 | 0,0 | 19,7 | 57,5 | [60-70] |

Associates | 29,7 | 42,9 | 57,1 | 71,0 | 77,7 | 101,8 | 136,1 | [100-200] |

Coop vendor | – 0,4 | 0,0 | 0,0 | – 2,3 | – 4,5 | – 8,9 | – 14,4 | – [20 – 30] |

DVDs Disposal | 3,8 | 0,5 | – 0,1 | 0,0 | 0,0 | 0,0 | 0,0 | [0 – 10] |

DVDs License fees | 0,4 | 0,2 | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | [0 – 10] |

DVDs Taxes | 0,3 | 0,1 | 0,0 | 0,0 | 0,0 | 0,0 | [0 – 10] | |

Editorial | 1,1 | 1,1 | 1,1 | 1,4 | 1,2 | 1,4 | 2,1 | [0-10] |

Free sample | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | [0 – 10] | |

Online adds | 0,0 | 0,0 | 0,1 | 0,2 | 2,6 | 9,4 | [20-30] | |

Promotions | 0,1 | 0,2 | 0,1 | 0,2 | 0,2 | 10,2 | 18,6 | [10-20] |

Research | 0,0 | 0,2 | 0,5 | 0,5 | 0,7 | 2,3 | 0,7 | [0 – 10] |

Sponsored links | 12,6 | 17,2 | 26,9 | 52,9 | 79,5 | 130,4 | 176,2 | [200-300] |

Synd Ad expense | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | 0,3 | [0-10] | |

Syndicated store | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | [0 – 10] | |

Others | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | 0,0 | [0 – 10] |

Total | 47,3 | 63,7 | 85,6 | 123,9 | 155,0 | 259,5 | 386,6 | [400-500] |

(EUR million) | ||||||||

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |

|---|---|---|---|---|---|---|---|---|

Advertising | 0,1 | 0,1 | – 0,1 | – 0,9 | 25,8 | 39,6 | [30-40] | |

Application Development Expense | 1,4 | [0-10] | ||||||

Customer Service | 10,9 | 18,5 | 17,7 | 22,2 | 54,7 | 47,7 | 74,6 | [100-200] |

Data Center | 14,0 | 24,4 | 27,8 | 27,7 | 35,1 | 67,7 | 107,4 | [100-200] |

Fulfillment Center | 106,6 | 175,0 | 188,3 | 228,1 | 313,1 | 576,3 | 973,0 | [1 000-1 500] |

Marketing | 27,9 | 50,1 | 24,2 | 28,3 | ||||

Operations | 0,1 | 0,0 | 0,0 | 0,2 | 0,2 | 0,2 | 0,2 | [0 – 10] |

Shared services center | 2,0 | 6,2 | [10-20] | |||||

Support Service | 0,2 | – 0,2 | 31,9 | 32,1 | 80,9 | 107,9 | 172,3 | [200-300] |

159,8 | 268,0 | 289,9 | 338,4 | 483,1 | 827,6 | 1 374,7 | [1 500 – 2 000] | |

(EUR thousand) | |||||||||

LuxSCS balance sheet | |||||||||

|---|---|---|---|---|---|---|---|---|---|

2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |

CAPITAL | |||||||||

Subscribed capital | 1 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | [0-10] |

Share premium | 116 204 | 417 587 | 417 587 | 417 587 | 417 587 | 417 587 | 464 363 | 549 035 | [500 000-600 000] |

Revaluation reserve | 690 | [400-500] | |||||||

Profit (loss) brought forward and of the financial year | – 149 362 | – 191 242 | – 26 127 | 275 480 | 684 473 | 1 125 172 | 1 426 951 | 1 544 845 | [1 500 000 – 2 000 000] |

CREDITORS | |||||||||

Amounts owed to affiliated companies | 33 185 | 171 406 | 25 525 | 26 292 | 28 013 | 37 549 | 65 931 | 138 006 | [100 000-200 000] |

Other creditors and accruals | 0 | 13 540 | 49 | 1 095 | 208 | 629 | 327 | 515 | [1 000-10 000] |

Total liabilities | 28 | 411 294 | 417 037 | 720 457 | 1 130 285 | 1 580 941 | 1 957 577 | 2 233 094 | [2 000 000-2 500 000] |

ASSETS | |||||||||

Shares in affiliated undertakings | 25 | 24 184 | 24 184 | 24 184 | 25 909 | 42 176 | 104 652 | 130 152 | [100 000-200 000] |

Intangible assets (acquired) and goodwill | 18 978 | 116 101 | [90 000-100 000] | ||||||

Amounts owed by affiliated companies | 0 | 387 053 | 392 810 | 696 227 | 1 104 283 | 1 538 640 | 1 833 863 | 1 986 763 | [2 000 000-2 500 000] |

Other debtors and cash | 3 | 57 | 42 | 47 | 93 | 125 | 84 | 79 | [300-400] |

Total assets | 28 | 411 294 | 417 037 | 720 457 | 1 130 285 | 1 580 941 | 1 957 577 | 2 233 094 | [2 000 000-2 500 000] |

(EUR thousand) | |||||||||

LuxSCS Profit and loss | |||||||||

|---|---|---|---|---|---|---|---|---|---|

2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | |

INCOME | |||||||||

Other operating income | 0 | 78 598 | 274 558 | 390 593 | 519 316 | 582 731 | 491 107 | 493 317 | [500 000 – 600 000] |

Interest receivable and similar income | 681 | 25 178 | 27 312 | 30 035 | 32 373 | 28 282 | 44 064 | 56 026 | [40 000 – 50 000] |

CHARGES | |||||||||

Other charges and other operating charges | 147 259 | 135 211 | 132 461 | 114 338 | 105 133 | 166 143 | 230 355 | 409 977 | [400 000 – 500 000] |

Value adjustments | 1 826 | 18 557 | [20 000 – 30 000] | ||||||

Interest payable and similar charges | 524 | 10 445 | 4 294 | 4 683 | 2 363 | 4 171 | 1 211 | 2 915 | [600 – 700] |

Profit of the financial year | – 147 101 | – 41 881 | 165 115 | 301 607 | 444 193 | 440 699 | 301 779 | 117 894 | [100 000 – 200 000] |

(EUR thousand) | |||||||||

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | ||

|---|---|---|---|---|---|---|---|---|---|

Description | Counterparty | ||||||||

Accounting fees | External | 2 | 3 | ||||||

Bank charges | External | 1 | 2 | 1 | 1 | 1 | 0 | 0 | [0-10] |

Courier charges | External | 0 | |||||||

Domain licenses | External | 285 | |||||||

Legal fees - general corporate | External | 111 | 232 | 537 | 617 | 875 | |||

Outside Services | External | 0 | |||||||

Miscellaneous gains/losses | Various | 0 | 0 | – 2 | 0 | ||||

Intercompany - sale of inventory | Amazon.de GmbH | 1 468 | |||||||

LuxOpCo | 2 205 | ||||||||

Amazon.co.uk Ltd | 522 | ||||||||

Buy-in payments | Amazon Technologies , & A9.com, & Audible | 68 271 | 42 274 | 27 209 | 9 439 | 39 957 | 26 803 | 56 975 | [1 000 – 10 000] |

Cost sharing agreement | Amazon Technologies , & A9.com, & Audible | 62 630 | 89 956 | 86 593 | 95 076 | 12 561 | 202 286 | 351 497 | [400 000 – 500 000] |

As further illustrated in Table 10, the costs borne by LuxSCS do not include any recharge of costs incurred by LuxOpCo related to the development, enhancement, or management of the Intangibles or recharge of any costs borne by LuxOpCo due to the operation of the EU on-line retail or service business, such as bad debts, inventory write-downs, marketing costs, etc. LuxSCS also did not incur any costs related to remuneration of the sole manager.

(in millions) | ||||||

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | |

|---|---|---|---|---|---|---|

Buy-In Payment (in USD) | 82,68 | 54,95 | 28,26 | 11,04 | 2,28 | 1,08 |

Buy-In Payment (EUR equivalent) | 68,34 | 42,27 | 19,15 | 8,45 | 2,40 | 0,79 |

(EUR million) | |||||||||

2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | Total | |

|---|---|---|---|---|---|---|---|---|---|

CSA Payment by LuxSCS | 63 | 90 | 87 | 95 | 125 | 202 | 351 | [400-500] | [1 000-1 500] |

No. | Functions of LuxSCS | Risks to be assumed by LuxSCS |

|---|---|---|

1 | [LuxSCS] shall conduct Development Program either directly or indirectly through its subsidiaries, within the European Territory and share the results of its activities with [A9 and ATI]. | All business risks relating to European Territory, including, but not limited to, credit risk, collections risk, market risk, risk of loss, risks relating to maintaining a workforce capable of efficiently and timely selling goods and providing services in the European Territory. |

2 | [LuxSCS] shall perform sales and marketing activities within the European Tenitory215. | Risk associated with the Development Program risks, including risk of failure or untimely development of products or provision of services for the European Territory. |

3 | [LuxSCS] shall perform strategic planning activities on customer needs and product requirements relating to Development Program within its Territory. | Products related market risks within the European Territory and impact on success of Research Program216 including:

|

4 | [LuxSCS] shall perform budgeting and planning activity associated with the Development Program. | Legal and regulatory risks associated with operating an on-line business. |

5 | [LuxSCS] shall manage strategic acquisitions of technologies that fall within the scope of the Development Program. | Brand development and brand recognition risks within the European Territory. |

6 | [LuxSCS] shall perform quality control and assurance functions. | Key personnel risks, quality control risks and product safety and liability risks (including warranty and liability risks) within the European Territory. |

7 | [LuxSCS] shall sell select, hire, and supervise employees, contractors and sub-contractors to perform any of the above activities. | Acquisition risks, including the ability to timely and successfully incorporate any acquired technology successfully. |

The second amendment, signed in February 2014 and effective as of 1 January 2014, changed the method to determine the share of the Development Costs to be borne by LuxSCS under the CSA. As a result, LuxSCS's cost share percentage is determined by the proportion of Amazon's gross profit attributable to Europe to the global group's gross profit in a given year.

More specifically, in its US income tax returns Amazon reported the Buy-In Payments received from LuxSCS under the Buy-In Agreement to receive the right to use pre-existing IP (the ‘Buy-In’) of around USD 217 million and CSA Payments received from LuxSCS under the CSA of around USD 116 million in 2005 and USD 77 million in 2006. The IRS contested both the amount of the Buy-In Payments and the CSA Payments. Based on an expert report dated 2011, the IRS considered USD 3,6 billion to be the correct amount of Buy-In Payments for the IP. This amount was adjusted to USD 3,468 billion by the IRS in the course of the court proceedings. The IRS expert used the discounted cash-flow method applied to the expected cash flows from the European business to arrive at that value. The assumptions on which that valuation was based deviated significantly from those of Amazon. In particular, the IRS experts considered Amazon's IP to have unlimited useful life, while Amazon considered it short-lived. As regards the CSA Payments, the IRS considered that 100 % of costs captured in the ‘Technology and Content’ cost centre should have been included in the pool of costs to be shared under the CSA.

To better understand the functions of LuxSCS and its subsidiaries in Europe in relation to the development, enhancement, management, and exploitation of the Intangibles, the Commission requested information produced in the context of the US Tax Court proceedings regarding the payments made by LuxSCS under the Buy-In Agreement and the CSA. Amazon submitted all information used and produced for the litigation before the US Tax Court to the Commission.

During the relevant period, LuxSCS received IP from affiliated companies and third parties at several instances which it, however, never acquired at its own initiative.

In other instances, the company holding the IP was acquired by another Amazon entity and its IP then transferred to ATI. This was the case when LuxOpCo acquired the [acquisition Q] group which held IP consisting not only of digital content rights, but also some technology. The technology component of the [acquisition Q] IP was sold to ATI, which then contributed it to the CSA in return for a buy-in payment from LuxSCS.

Date | Type of decision | Summary | |

|---|---|---|---|

07/06/2004 | Written resolution of the sole manager of LuxSCS ([…]as proxyholder) | Approving all necessary actions as regard the post-formation steps; Ratification of the opening of the bank account with [bank]; Approving entering into a domiciliation agreement with [service company]; Incorporation of LuxOpCo. | |

14/01/2005 | Written resolution of the sole manager of LuxSCS ([…] as vice President) | Ratification of two cost sharing agreements and a buy-in agreement; Adopting amendments to LuxSCS' articles of association, in order to resolve the adoption of certain specific rights of the shares on dividends and other distributions, and the adoption of specific share premium accounts; Increase of LuxSCS' share capital by way of an all assets and liabilities contribution to be undertaken by ACI Holdings Limited, a Gibraltar company (‘ACI’); Approving the appointment of […] as additional manager of LuxOpCo and an amendment of the corporate object of LuxOpCo; Assigning a note receivable to Amazon.com International Sales, Inc.; Granting a loan to LuxOpCo. | |

17/01/2005 | Minutes of extraordinary General Meeting ([…] as president, […] as secretary, […] as scrutineer) | Adoption of new articles of association, in order to resolve the adoption of some specific rights of the shares on dividends and other distributions; Increase of share capital | |

07/06/2005 | Written resolution of the sole manager of LuxSCS ([…] as vice President) | Transfer of the registered address of LuxSCS. | |

22/06/2005 | Minutes of General Meeting ([…] as president, […] as secretary, […] as scrutineer) | Waiver of notice of rights; Approval of the annual accounts as of 31 December 2004; Discharge of the sole manager, Amazon Europe Holding, Inc. for the financial year ending on 31 December 2004. | |

22/06/2005 | Written resolution of the sole manager of LuxSCS ([…] as vice president) | Settlement of LuxSCS's accounts as of 31 December 2004 and resolution to submit such accounts to the LuxSCS's shareholders for approval; Discharge of the sole manager of LuxSCS for the accounting year ending on 31 December 2004. | |

06/02/2006 | Written resolution of the sole manager of LuxSCS ([…] acting on behalf) | Adopting an increase of the share capital of LuxSCS by a contribution in kind of shares held by Amazon.com, Inc. in Amazon.fr Holdings SAS having a value of USD 1 017 240 in consideration of limited shares of LuxSCS; Approving the entering into one or more share transfer agreements in order to acquire 100 % off the shares of Amazon.co.uk Ltd and Amazon.de GmbH held by Amazon.com, Inc. and 95,8 % of the shares of Amazon.fr Holdings SAS held by Amazon.com, Inc., in consideration of a promissory note in principal amount of USD 194 672 760,0; Adoption of increase of the share capital by way of an all assets and liabilities contribution to be undertaken by ACI Holdings in consideration of limited shares of LuxSCS. | |

06/02/2006 | Minutes of the extraordinary General Meeting of LuxSCS ([…] as president, […] as secretary, […] as scrutineer) | Increase of the share capital of LuxSCS; Resolution to accept the subscription and payment by Amazon.com, Inc. of new limited shares by way of a contribution in kind; Increase of the share capital of LuxSCS; Subscription and payment by ACI Holdings Limited of new limited shares by way of a contribution in kind; Cancellation of 900 limited shares in LuxSCS; New composition of the shareholding of LuxSCS. | |

07/02/2006 | Written resolution of the sole manager of LuxSCS ([…] acting on behalf) | Approving the entering into share transfer agreement in order to sell 100 % of the shares of Amazon.de GmbH and 8 724 191 of the shares (representing 93,1471 %) of Amazon.co.uk Ltd, in consideration of a note amounting to EUR 136 828 362; Proposal to contribute 6,8529 % of the shares of Amazon.co.uk Ltd and 100 % of the shares of amazon.fr Holdings SAS to LuxOpCo,; Granting a loan to LuxOpCo. | |

18/04/2006 | Written resolution of the sole manager of LuxSCS ([…] acting on behalf) | Resolution to split into three different promissory notes a promissory note issued by the LuxSCS on February 6, 2006 in the principal amount of USD 194 672 760 to the benefit of Amazon.com. Inc.; Increase the share capital of LuxSCS by a contribution in kind to LuxSCS by ACI of the UK Note and the DE Note in consideration of the issuance of limited shares of LuxSCS. | |

19/04/2006 | Minutes of the extraordinary General Meeting of LuxSCS ([…] as president, […] as secretary, […] as scrutineer) | Increase of the share capital of LuxSCS; Resolution to accept subscription and payment by Amazon.com, Inc. of new limited shares by way of contribution in kind; New composition of LuxSCS; Amendment of the articles of association. | |

28/04/2006 | Written resolution of the sole manager of LuxSCS ([…] as vice president) | Acknowledgement of the resignation of […]as manager of LuxOpCo and of the appointment of […] and […] as managers of LuxOpCo; Adopting an increase of the share capital of [LuxSCS] by way of an all assets and liabilities contribution to be undertaken by ACI Holdings Limited, a Gibraltar company (‘ACIH’) in consideration of limited shares of LuxSCS; Approving the assignment of certain IP rights from Amazon.co.uk Ltd, Amazon.fr Holdings SAS and Amazon.de GmbH; Approving the acquisition of the EU Retail Business of Amazon.com Int'l Sales, Inc., and the subsequent transfer of the same to LuxOpCo; Approving intellectual property license agreements with LuxOpCo; Merger of certain limited shareholders of LuxSCS; Loan to LuxOpCo. | |

28/04/2006 | Minutes of the extraordinary General Meeting of LuxSCS ([…] as president, […] as secretary, […] as scrutineer) | Increase of share capital; Resolution to accept subscription and payment by ACI Holdings Limited of all the 3 750 limited shares; Cancellation of 1 993 shares; New composition of the shareholding of LuxSCS; Amendments of the articles of Association. | |

09/05/2006 | Minutes of the General Meeting of LuxSCS ([…] as president, […] as secretary, […] as scrutineer) | Waiver of notice rights; Amendment to the articles of association of LuxSCS further to the merger of Amazon.com Int'l Marketplace, Inc. into Amazon Int'l Sales. | |

27/06/2006 | Minutes of the extraordinary General Meeting of LuxSCS ([…] as president, […] as secretary, […] as scrutineer) | Decrease of the personal share premium account of ACI Holdings limited further to the final valuation of the 28 April 2006 contribution. | |

22/05/2007 | Written resolution of the shareholders of LuxSCS ([…] as vice President, […] as vice president, […] as treasurer and director) | Settlement of LuxSCS' annual accounts as of 31 December 2005 and resolution to submit the annual accounts to the sole shareholder of LuxSCS and to discharge the sole manager of LuxSCS for the accounting year ending on 31 December 2005. | |

22/05/2007 | Written resolution of the shareholders of LuxSCS ([…] as vice President, […] as vice president, […] as vice president, treasurer and director) | Approval of the annual accounts as of 31 December 2005 and allocation of the result; Discharge of the managers for the financial year ending on 31 December 2005. | |

25/04/2008 | Written resolution of the sole manager of LuxSCS ([…] as vice president) | Settlement of LuxSCS's annual accounts as of 31 December 2006 and resolution to submit such annual accounts to LuxSCS's shareholders for approval; Resolution to discharge to the sole manager of LuxSCS for the accounting year ending on 31 December 2006. | |

25/04/2008 | Written resolution of the shareholders of LuxSCS ([…] as vice President, […] as vice president, […] as vice president, treasurer and director) | Approval of the annual accounts as of 31 December 2006 and allocation of the result and resolution to submit the annual accounts to the shareholders of LuxSCS; Discharge of the sole manager of the manager for the financial year ending on 31 December 2006. | |

18/06/2008 | Written resolution of the sole manager of LuxSCS ([…] as vice President) | Approval of the annual accounts as of 31 December 2006 of LuxOpCo and amendment and adoption of its signatory delegation policies; Approval of the annual accounts as of 31 December 2006 of Amazon Eurasia Holdings Sarl (‘AEH’) and amendment and adoption of its signatory delegation policies. | |

23/03/2009 | Written resolution of the sole manager of LuxSCS ([…] as vice president) | Resolution to contribute an aggregate amount of EUR 25 000 to AEH in consideration for the issuance of new shares by AEH. | |

25/06/2009 | Written resolution of the shareholders of LuxSCS ([…] as vice president, […] as president, […] as vice president, treasurer and director) | Approval of the annual accounts as of 31 December 2008 and allocation of the result; Discharge of the sole manager of the manager for the financial year ending on 31 December 2008. | |

25/06/2009 | Written resolution of the sole manager of LuxSCS ([…] as president) | Settlement of LuxSCS's annual accounts as of 31 December 2009 and resolution to submit such annual accounts to LuxSCS's shareholders for approval; Proposal to give discharge to the sole manager of LuxSCS for the accounting year ending on 31 December 2008; Approval of the annual accounts as of 31 December 2008 of LuxOpCo; Approval of the annual accounts as of 31 December 2008 of AEH; Proposal to increase the share capital of AEH by a contribution in cash. | |

06/07/2009 | Written resolution of the sole manager of LuxSCS ([…] as president, […] as vice president, […] as vice president, treasurer and director) | Approval of the annual accounts as of 31 December 2008 and allocation of the result; Discharge of the sole manager of the manager for the financial year ending on 31 December 2008. | |

31/08/2009 | Written resolution of the sole manager of LuxSCS ([…] as president) | Convening of an extraordinary general meeting of LuxSCS regarding from 1 September 2009 regarding: Waiver of notice rights; Amendment to the articles of association of LuxSCS further to the liquidation of ACI Holdings Limited and the related transfer of its 3 750 limited shares held in LuxSCS to its parent company Amazon.com Int'l Sales, Inc. | |

11/09/2009 | Minutes of the General Meeting of LuxSCS ([…] as president, […] as secretary, […] as scrutineer) | Waiver of notice rights; Amendment to the articles of association of LuxSCS further to the liquidation of ACI Holdings Limited and the related transfer of its 3 750 limited shares held in LuxSCS to its parent company Amazon.com Int'l Sales, Inc. | |

07/12/2009 | Written resolution of the sole manager of LuxSCS ([…] as president) | Resolution on increase of the share capital of AEH by a contribution in cash. | |

22/12/2009 | Written resolution of the shareholders of LuxSCS ([…] as president, […] as vice president, […] as vice president and treasurer) | Approval of the distribution of interim dividends of LuxSCS. | |

22/12/2009 | Written resolution of the sole manager of LuxSCS ([…] as president) | Distribution of an interim dividend to the Shareholders of LuxSCS. | |

30/04/2010 | Written resolution of the sole manager of LuxSCS ([…] as president) | Approval of LuxOpCO's annual accounts as of 31 December 2009; Approval of AEH's annual accounts as of 31 December 2009. | |

28/05/2010 | Written resolution of the sole manager of LuxSCS ([…] as president) | Settlement of LuxSCS' annual accounts as of 31 December 2009 and resolution to submit it to the shareholders of LuxSCS and to discharge the sole manager of LuxSCS for the accounting year ending on 31 December 2009; Acknowledgement of the change of registered office of LuxSCS' shareholders and sole manager. | |

14/06/2010 | Written resolution of the shareholders of LuxSCS ([…] as president, […] as vice president, […] as vice president and treasurer) | Approval of the annual accounts as of 31 December 2009 and allocation of the result; Discharge of the sole manager for the financial year ending on 31 December 2009. | |

05/07/2010 | Written resolution of the sole manager of LuxSCS ([…] as president) | Ratification of shareholder's advances in cash made by the LuxSCS to AEH; Approval of increase the share capital of AEH by way of a contribution in kind of a receivable. | |

13/12/2010 | Written resolution of the sole manager of LuxSCS ([…] as president) | Ratification of shareholder's advances in cash made by the LuxSCS to AEH; Proposal to increase the share capital of AEH by way of a contribution in kind of a receivable; Powers of attorney to […], […] and […] to act on behalf of LuxSCS in this respect. | |

07/04/2011 | Written resolution of the shareholders of LuxSCS ([…] as president, […] as vice president) | Approval of the allocation of the EUR equivalent of GBP 41 M to a special reserve of LuxSCS further to the contribution by Amazon.com Int'l Sales, Inc., of 3 115 shares it holds in Video Island Entertainment Ltd | |

07/04/2011 | Written resolution of the shareholders of LuxSCS ([…] as president) | Resolution to recommend to the shareholders of LuxSCS the allocation of the EUR equivalent of GBP 41 M to a special reserve of LuxSCS further to the contribution by Amazon.com Int'l Sales, Inc., of 3 115 shares it holds in Video Island Entertainment Ltd; Approval of the contribution by LuxSCS to its wholly owned subsidiary LuxOpCo of 3 115 shares held in video Island Entertainment Limited. | |

23/05/2011 | Written resolution of the shareholders of LuxSCS ([…] as president, […] as vice president, […] as vice president and treasurer) | Approval of the annual accounts as of 31 December 2010 and allocation of result; Discharge of the sole manager for the financial year ending on 31 December 2010. | |

23/05/2011 | Written resolution of the sole manager of LuxSCS ([…] as president) | Settlement of LuxSCS 's annual accounts as of 31 December 2010 and resolution to submit such annual accounts to the LuxSCS's shareholders for approval; Proposal to give discharge to the sole manager of LuxSCS for the accounting year ending on 31 December 2010. | |

01/07/2011 | Written resolution of the sole manager of LuxSCS ([…] as president) | Ratification of a shareholder's advance in cash made by LuxSCS to AEH; Approval, as sole shareholder, of the increase of the share capital of AEH by way of a contribution in kind of a receivable. | |

25/01/2012 | Written resolution of the sole manager of LuxSCS ([…] as president) | Acknowledgement of the resignation of Mr […] as manager of LuxOpCo and AEH approval of the granting of discharge; Acknowledgement of the appointment of Mr […] as new manager of LuxOpCo and AEH; Approval of the amendment of the corporate signatory policy of LuxOpCo and AEH; Ratification of the shareholder's advance in cash made by the sole shareholder to LuxSCS; Approval of the increase of the share capital of AEH by way of a contribution in kind of a claim; Ratification of the entering by the LuxSCS into amended and restated credit facility agreement; Ratification of the entering by the LuxSCS into an IP assignment agreement dated March 28, 2011 with [acquisition Q]. | |

23/04/2012 | Written resolution of the sole manager of LuxSCS ([…] as president) | Settlement of LuxSCS' annual accounts as of 31 December 2011 and discharge of the sole manager of LuxSCS for the accounting year ending on 31 December 2011; Approval as shareholder of LuxOpCo of the annual accounts as of 31 December 2011; Approval as shareholder of AEH of the annual accounts as of 31 December 2011. | |

27/04/2012 | Written resolution of the shareholders of LuxSCS ([…] as president, […] as vice president, […] as vice president and treasurer) | Approval of the annual accounts as of 31 December 2011 and allocation of the result; Discharge of the sole manager for the financial year ending on 31 December 2011. | |

27/08/2012 | Written resolution of the sole manager of LuxSCS ([…] as president) | Approval of the resignation of Mr […] as manager of LuxOpCo and AEH; Approval of the appointment of Mr […] and Mr […] as new managers of LuxOpCo and AEH and the amendment of the corporate signatory delegation policy of LuxOpCo and AEH; Ratification of the shareholder's advance in cash made by LuxSCS to AEH; Approval of an increase of the share capital of AEH by way of a contribution in kind. | |

12/12/2012 | Written resolution of the sole manager of LuxSCS (represented by […] by virtue of a delegation of authority) | Ratification of the appointment of Mr […] as new manager of LuxOpCo and AEH; Approval of the amendment of the corporate signature policy of LuxOpCo and AEH; Approval of the resignation of Mr […] as manager of LuxOpCo and AEH. | |

02/04/2013 | Written resolution of the sole manager of LuxSCS (represented by […] by virtue of a delegation of authority) | Settlement of LuxSCS' annual accounts as of 31 December 2012 and discharge of the sole manager of LuxSCS; Approval as shareholder of AEH of the annual accounts as of 31 December 2012; Approval as shareholder of LuxOpCo of the annual accounts as 31 December 2012; Ratification of the entry by LuxSCS into an asset purchase agreement for the acquisition of certain assets from [acquisition W1] and [acquisition W2]; Approval of the entering by LuxSCS into an amendment to an IP assignment agreement with Elkotob.com LLC. | |

08/04/2013 | Written resolution of the shareholders of LuxSCS (represented by […] by virtue of a delegation of authority, […] as vice president, […] as vice president and treasurer) | Approval of the annual accounts as of 31 December 2012 and allocation of the result; Discharge of the sole manager for the financial year ending on 31 December 2012. |

As illustrated in Table 14, the written resolutions of the sole manager, and the minutes from general meetings of LuxSCS from its incorporation in 2004 to 2013 indicate that the sole manager and the partners of LuxSCS principally dealt only with topics related to the monitoring of their investments in their capacity as partners in LuxSCS, such as share capital changes, capital contributions, granting of loans to affiliated companies and other financial decisions related to LuxSCS and its subsidiaries. The decisions reflected in the written resolutions and minutes also concerned the appointments of managers in the subsidiaries, their discharge and resignations, amendments of articles of association and approval of the accounts.

On 14 January 2005, the sole manager of LuxSCS approved and ratified that LuxSCS had already entered into the Buy-In Agreement and two cost sharing agreements (including the CSA) during December 2004 and January 2005.

On 28 April 2006, within the context of the reorganisation of the European retail operations, the sole manager of LuxSCS approved the assignment of the editorial contents, trademarks and domain names from Amazon.co.uk Ltd, Amazon.fr Holding SAS and Amazon.de GmbH to LuxSCS as well as the conclusion of the License Agreement with LuxOpCo. The sole manager was further authorised to execute those agreements.

On 25 January 2012, the sole manager of LuxSCS approved and ratified the IP assignment agreement with [acquisition Q] as entered into by LuxSCS and effective as of 29 March 2011. The sole manager was further authorised to execute the IP assignment agreement.

On 2 April 2013, it was reported that LuxSCS and ATI had entered into an asset purchase agreement dated 1 March 2013 to acquire certain assets from a third party comprising software codes and all related intellectual property rights. The sole manager of LuxSCS ratified the asset purchase agreement and the license to LuxOpCo.

The M.com Agreements referred to in the TP Report are described in more detail in Recitals 223 to 229.

(USD) | ||||||

Variable unit fees (USD/units) | Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 6 |

|---|---|---|---|---|---|---|

Sortable | 2,36 | 2,36 | 2,10 | 1,87 | 1,78 | 1,78 |

Conveyable | 3,83 | 3,83 | 3,57 | 3,27 | 3,13 | 3,13 |

Non-sortable or non-conveyable | 4,83 | 4,83 | 4,81 | 4,48 | 4,28 | 4,28 |

Drop-ship units | 0,75 | 0,75 | 0,75 | 0,75 | 0,75 | 0,75 |

[…] Gift Card Drop-Ship Units | 0,75 | Gift Card free | ||||

Customer Return Processing | Same as variable unit fee for each such […] product returned to Amazon or its affiliates | |||||

Vendor Return Processing | 1,00 | 1,00 | 1,00 | 1,00 | 1,00 | 1,00 |

(%) | ||||||

Year 1 | Year 2 | Year 3 | Year 4 | Year 5 | Year 6 | |

|---|---|---|---|---|---|---|

Product Sales Commission (other than catalogue-branded […] products) | 5,0 | 5,0 | 4,5 | 4,0 | 4,0 | 4,0 |

Additional Apparel Product Sales Commission | 2,5 | 2,5 | 3,0 | 3,5 | 3,5 | 3,5 |

Product Sales Commission (catalogue-branded […] products) | 2,0 | 2,5 | 2,5 | 2,5 | 3,0 | 3,0 |

For its part, Amazon was to pay [A] a referral fee for Amazon products displayed for sale on the [A] website. This fee amounted to 5 % on sales in 2001 and 2002, 4,5 % on sales in 2003, and 4 % on sales from 2004 to 2006.

Under the [I] Agreement, Amazon did not provide an e-commerce platform for [I], but agreed that [I] products would be listed for sale and integrated into the search and browse features of the Amazon website. [I] was to pay a remuneration of 8 % to 9 % of sales generated via the Amazon website.

Amazon submitted all IP license agreements concluded with third parties since 2000. None of those agreements concerned a transfer of IP comparable to that in the License Agreement. The agreements submitted do not cover any transfer of the Amazon trademark, e-platform technology or customer database. They concern either the licensing of a registered patent or the digital content.

In May 2014, Amazon received a new tax ruling from the Luxembourg tax administration concerning changes made to its corporate and tax structure in Luxembourg. Under the new corporate structure, the role of LuxSCS […]. The principal change to that structure was the creation of a new […] company […], which was inserted in the existing structure between […].

- (1)The lower listing fee ‘reflects the […] financial situation and outlook [description of the state of the Retail business market and Amazon's strategy]’262.

- (2)[Description of Amazon's commercial strategy]. If […] were to charge a listing fee of [4-6] % to cover its costs of providing the platform service [Amazon projections], both of which would be detrimental to […]. On the other hand, the discount […] will be required to grant will be limited by […]. Given that the allocation of technology and platform expenses is about [4-6] percent of LuxOpCo's projected retail revenues in 2014 it is […]. Thus, a listing fee that is less than [4-6] percent would appear to be a better alternative for LuxOpCo than LuxOpCo investing in the technology and platform itself263.

Under the new corporate structure, the role of ASE remains unchanged. It will continue to operate and manage the European Marketplace business. Instead of paying a royalty to LuxOpCo for the totality of sub-licensed Intangibles, it now pays a […] fee […].

The role of the EU Local Affiliates also remained unchanged the under new corporate structure.

The ordinary rules of corporate taxation in Luxembourg are to be found in the Luxembourg Corporate Income Tax Code (loi modifiée du 4 décembre 1967 concernant l'impôt sur le revenue, the ‘LIR’).

Article 18(1) LIR provides the method to establish a corporate taxpayer's annual profit: ‘The profit is determined as the difference between net assets as of the end and net assets as of the beginning of the reporting period, increased by the withdrawals of business cash or other assets by the taxpayer for its personal use or any other uses which are not intended in the interests of the company and decreased by additional contributions performed during the reporting period’.

As of 1 January 2017, a new article 56bis LIR explicitly formalises the application of the arm's length principle under Luxembourg tax law. With the effect of the same date, the above mentioned Circulars were replaced by the Circulaire du directeur des contributions LIR no 56/1 – 56bis/1 du 27 décembre 2016.

When independent companies transact with each other on the market, the conditions of that transaction, including the prices of the goods transferred or the services provided, are normally determined by external market forces. When companies integrated in a multinational corporate group transact with companies from the same group (‘associated group companies’), their commercial and financial relations may not be determined by external market forces, but may, in some cases, be influenced by a common interest to minimise the tax liabilities of the group.

The CUP method, the TNMM and the profit split method are relevant for the present Decision and are therefore described in more detail in Recitals 253 to 256.

The 2010 JTPF Report further found that, based on the experience of the national tax administrations, an appropriate mark-up for low value adding services would typically fall within a range of 3 % to 10 %, and often around 5 %. However, where the facts and circumstances of the specific transaction support a different mark-up, that should be taken into consideration.

A brief overview of financial indicators and accounting concepts frequently used in this Decision is given below.

A typical profit and loss account first records the income that a company receives from its normal business activities, usually from the sale of goods and services to customers. This accounting item is referred to as ‘Sales’ or ‘Turnover’ or ‘Revenue’.

Cost of goods sold (‘COGS’) represents mainly the value of material used for the production of goods (raw materials) or the purchase price of goods that have been resold if the company does not process the goods sold. COGS is deducted from sales to calculate gross profit.

Sales (or Turnover or Revenue)

Cost of goods sold (COGS)

Gross Profit

Operating Expense (OpEx)

Operating profit (EBITDA)

Earnings before interest and taxes (EBIT) or operating income

Interest and and exceptional or extraordinary income

Taxable income

Tax

Net profit

Performance and profitability is often measured using ratios presented as ‘margins’ or ‘mark-ups’. Margins are also used in peer comparisons in transfer pricing.

In transfer pricing, gross margins can be calculated as gross profit divided by sales (or COGS), and net margins as the operating profit divided by sales (or total costs, i.e. sum of COGS and Operating Expenses), in particular when the transactional net margin method is used. Therefore, when using the ‘net margin’ method the numerator of the profit level indicator would be the operating profit.

First, the Commission criticised the fact that the contested tax ruling appeared to have been granted in the absence of a transfer pricing report. It further observed that the ruling had been granted within eleven working days from the receipt of the first letter constituting the ruling request.