Commission Decision

of 11 December 2007

on the State aid case C 53/06 (ex N 262/05, ex CP 127/04), investment by the city of Amsterdam in a fibre-to-the-home (FttH) network

(notified under document number C(2007) 6072)

(Only the Dutch version is authentic)

(Text with EEA relevance)

(2008/729/EC)

THE COMMISSION OF THE EUROPEAN COMMUNITIES,

Having regard to the Treaty establishing the European Community, and in particular the first subparagraph of Article 88(2) thereof,

Having regard to the Agreement on the European Economic Area, and in particular Article 62(1)(a) thereof,

Whereas:

In April 2004, the municipality of Amsterdam contacted the Commission regarding the public procurement aspects of the roll-out of a FttH (fibre-to-the-home) telecommunications access network. In addition, the municipality requested the Commission to confirm that the project did not entail State aid within the meaning of Article 87(1) of the EC Treaty. By letter of 22 July 2004, the Commission informed the municipality of Amsterdam that such a confirmation can only be given after a notification of the measure by the Dutch authorities. The Commission requested the Dutch authorities on 23 July 2004 to provide any information necessary for an assessment of the measure under Article 87(1) of the EC Treaty. The Dutch authorities asked for an extension of the deadline in August 2004 which was accepted by the Commission on 7 September 2004.

In September 2004, the Dutch authorities convened with the Commission to present and discuss the plans of the municipality of Amsterdam. On 7 October 2004, the authorities stated in their reply to the Commission’s letter of 23 July 2004 that the project in Amsterdam would be notified in the near future. On 17 May 2005, the Dutch authorities notified the project — the participation of the municipality of Amsterdam in an undertaking carrying out the roll-out and owning this network. The Dutch authorities were seeking confirmation from the Commission that the investment of the municipality of Amsterdam in the legal entity owning the network is in line with the Market Economy Investor Principle (‘MEIP’) and accordingly does not constitute State aid.

Following further information sent by the authorities on 23 June 2005, and a meeting which took place on 28 June 2005 between representatives of the city of Amsterdam and the Commission, the Commission sent on 15 July 2005 a letter containing elements of an explanation of the application of the MEIP together with a second request for information.

The Dutch authorities stated in a letter, registered on 18 November 2005, that there was a delay in the planning and that the municipality of Amsterdam was still working on the setup of the project and the investment conditions. The Dutch authorities declared that they would need more time in order to provide the requested information and asked the Commission to suspend the assessment until all data would be available.

The municipality of Amsterdam informed the Commission by e-mail registered on 23 December 2005 that the City council of Amsterdam had by unanimity decided to invest in the roll-out of the FttH network and stated further that negotiations with BAM/DRAKA (for the construction of the network) and with BBned (for the exploitation of the network) and the negotiations with ING RE and five housing corporations (co-investors) were all on track and would be finalised by January 2006.

On 3 March 2006, the Commission sent a reminder to the Dutch authorities, referring to the statement of the Dutch authorities in November 2005 that further information would be provided once further progress had been made on the setup of the project and which was foreseen for spring 2006. The Commission also reminded the Dutch authorities of the standstill obligation of Article 88(3) of the EC Treaty.

UPC requested the District Court in Amsterdam in a procedure for interim measures to order the municipality of Amsterdam to respect the standstill obligation laid down in Article 88(3) of the EC Treaty and not to continue the project before the Commission has finalised its assessment. The request by UPC was dismissed by the District Court which stated in its judgement of 22 June 2006 that it was not obvious that the municipality’s involvement in the project involved State aid. According to the Court, the mere fact that the municipality has initiated the project is not to be considered as State aid. Moreover, the Court concluded that the initial costs incurred by Amsterdam (studies, etc.) would be reimbursed by the joint-venture Glasvezelnet Amsterdam CV and therefore did not constitute aid.

By letter dated 20 December 2006, the Commission informed the Netherlands that it had decided to initiate the procedure laid down in Article 88(2) of the EC Treaty in respect of the notified measure.

By letter of 8 January 2007, the Dutch authorities requested access to several documents submitted by UPC mentioned in the opening decision. By letter registered on 13 February 2007, UPC agreed to share the requested documents with the Dutch authorities, which were forwarded by the Commission to the authorities.

The Dutch authorities responded by letter registered on 16 March 2007 to the Commission’s decision to open the formal investigation procedure.

The Commission services met with representatives of Liberty Global/UPC on 5 July 2007 and with the Dutch authorities on 5 November 2007. The Dutch authorities submitted additional information on 9 November 2007 and on 12 November 2007.

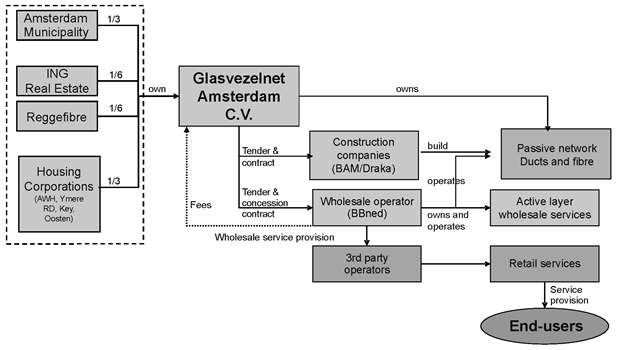

The planned FttH network in Amsterdam will serve 37 000 households in Amsterdam in the districts of Zeeburg, Osdorp and Oost-Watergraafsmeer, which comprise together about 10 % of the city of Amsterdam. The municipality of Amsterdam also expressed its long-term ambition to extend the project to other parts of Amsterdam, with up to 400 000 household connections altogether. However, this potential extension is not part of the project under assessment.

The first layer is the so-called ‘passive network infrastructure’, which includes ducts, fibre and street cabinets.

This passive infrastructure is activated by means of telecommunications equipment (the second or ‘active layer’) by a wholesale operator managing and maintaining the network and providing wholesale services to retail operators. The active layer includes the management, control and maintenance systems necessary to operate the network, such as switches, routers or splitters.

The wholesale operator will provide an open, non-discriminatory access to retail operators to offer television, broadband, telephony and other Internet-based services to end customers (third or ‘retail layer’). In order to be able to provide these services, retail service providers will have to invest, inter alia, in equipment, procure content and operate their own service platform (maintenance, customer care, and billing).

Taking also into account these difficulties encountered, the impact of potential State aid on the investments of private operators, the opening of procedure was also justified because the Dutch authorities did not submit to the Commission all information necessary to assess the project.

Finally, the Commission initiated the formal investigation procedure also in order to give the Dutch authorities and third parties the opportunity to submit their comments on its provisional assessment of the measure described and to make available to the Commission any relevant information related to the measure.

As regards the commercial viability of the project, UPC argues that the new fibre network would not enable operators to offer significantly different services from the services offered by the current operators. Consequently, and taking into account that the broadband penetration in the areas to be covered by GNA has already reached 65 % of the households, the new fibre network would fail to attract enough customers for its services to make its business plan viable.

Furthermore, UPC also expresses doubts as to whether the public investment in GNA is made on equal terms with the investments of the other shareholders of GNA. UPC argues that the fact that the municipality of Amsterdam undertook certain pre-investments and other GNA shareholders decided to commit themselves to participate in the project after the municipality performed certain feasibility studies indicates that the investment was not pursued on equal terms by all the shareholders which would shed further doubts on the market conformity of the measure.

The comments submitted by COM HEM, a Swedish cable operator, take a similar line to the other operators. COM HEM generally doubts the market conformity of the investment of the Amsterdam municipality. In its observations, COM HEM argues that public funding for broadband projects in urban areas are seldom in line with the MEIP and have strong distortive effects on competition. COM HEM also calls for a strict application of the MEIP and highlights the precedent value of the Amsterdam case to future municipal and other public sector investments.

Another party requiring anonymity, which provides telecommunications services in several European countries, welcomed the Commission decision to initiate the formal investigation procedure. The company argues that its investment is endangered by the initiatives of municipalities using public funds which have a distortive effect on the market. The company expects the Commission to ban any public money in the Citynet Amsterdam project.

By letter registered on 16 March 2007, the Dutch authorities submitted their comments in connection with the Commission’s decision to initiate the formal investigation procedure. Furthermore, the Dutch authorities also provided comments on non-confidential versions of the studies prepared for UPC by RBB.

Throughout their submissions, the Dutch authorities maintain their position that the investment of the municipality of Amsterdam in GNA is in line with the MEIP and therefore does not constitute State aid.

The authorities also emphasise the pro-competitive business model of GNA, which provides — contrary to the closed model of cable operators — open and non-discriminatory access to all retail operators. They argue that the new business model, inter alia, promotes service competition, boosts innovation and helps to reduce the risk of service providers by allowing them to use funding which matches the characteristics of each individual layer.

The Dutch authorities take the view that the shareholders of the project provide further evidence that the GNA project is pursued on market terms. In this respect, the authorities emphasize the fact that two private investors and the commercial subsidiaries of the housing corporations are willing to participate in the project under the same terms and conditions as the municipality. They also refer to the open tender procedures for the construction of the network and for the wholesale service provision of the network. They further highlight that the fact that a significant bank loan was offered to GNA on market terms constitutes clear evidence that the project and the underlying business plan are based on prudent market terms.

Regarding the pre-investments by the municipality of Amsterdam, the Commission noted in the opening decision that the municipality took initiatives before establishing GNA which seemed to go beyond what normal market practice would suggest. The Commission expressed concerns that the pre-investments might have reduced the risks associated with the project for all investing parties. Some of the start-up risk of the business underlying the GNA business plan might have been absorbed or mitigated by the municipality of Amsterdam before the investments by ING and Reggefiber in GNA were made. Based on the information submitted by the Dutch authorities before the opening of the formal investigation, it could not be clarified whether all shareholders in GNA did invest under the same terms and conditions.

In their reply, the Dutch authorities underline that all investors committed themselves on 24 May 2006 to the investment in GNA on identical terms and conditions.

As regards the pre-investments (reaching the amount of EUR […]), the Dutch authorities claim that it has always been the understanding of all GNA shareholders that the pre-investments by the municipality of Amsterdam would have to be repaid by GNA. To support this assertion, the Dutch authorities distinguish between two parts in the pre-investments.

As regards the first part, the Dutch authorities stress that, although the agreements establishing the GNA were only signed on 24 May 2006 binding all parties to the EUR […] investment, in the letters of intent of […], the future GNA shareholders decided together to earmark a lump sum of EUR […] (ex. VAT) for the preparation costs of the project. Amongst others, this amount also covered the costs of the tender procedures for the selection of the builder of the network (BAM/Draka) and for the wholesale operator (BBNed), certain costs related to the notification procedure and certain digging activities.

As for the second part of the pre-investments (amounting to EUR […]), the Dutch authorities argued that such pre-investments are fully in line with normal market practice: prudent market investors would follow the same practice in joint projects as one of the parties usually has to take on the role of ‘lead investor’. The authorities also stressed that pre-investments by the municipality of Amsterdam did not reduce the start-up risk of the investment for the other GNA shareholders.

The Dutch authorities also argue that the pre-investments did not provide any advantage to any party, therefore could not constitute State aid within the meaning of Article 87(1) of the EC Treaty. For instance, the start of certain digging activities was triggered by the fact that some civil works took place in areas which were important for the future construction of the GNA network. Since all digging activities are coordinated in Amsterdam, digging just a few months afterwards would have been impossible, which would have caused delays and additional costs for GNA.

Furthermore, the Dutch authorities claim that all these costs were incorporated in the business plan and that no new cost elements emerged that would not have been known by the other GNA shareholders.

Furthermore, the Dutch authorities do not consider their own feasibility studies as part of the pre-investments. According to the Dutch authorities, all prudent market investors would carry out such studies. The Dutch authorities argue that these studies could not have reduced or absorbed some of the start-up risk for the other GNA shareholders, as the other potential shareholders have to follow their own appraisal as well and assess their own risks and benefits from the project.

Similarly, the feasibility studies of the other GNA shareholders (such as ING RE’s or Reggefiber’s) carried out before investing into GNA were financed by the respective parties without being charged to GNA.

Therefore, the Dutch authorities assert that the preliminary doubts of the Commission regarding ‘concomitance’ and ‘identical terms and conditions’ originating from the pre-investments of the Amsterdam municipality are properly addressed by the above-mentioned explanations provided and by the reimbursement of the relevant pre-financed costs to GNA.

With regard to GNA’s business plan, the Dutch authorities argue that investments made by public authorities satisfy the conditions of the MEIP if they are pursued under the same terms and conditions as those made by private investors. The presence of private investors should guarantee that the project is done on market terms. Therefore, they argue that it was not strictly necessary for the Commission to analyse GNA’s business plan.

Second, the Dutch authorities consider that all assumptions of GNA’s business plan were not optimistic, rather conservative ones.

Regarding the targeted penetration rate, in the opening decision, the Commission came to the preliminary conclusion that, based on the available data, achieving at least […] % penetration for GNA’s ‘minimum scenario’ seems optimistic. Moreover, the target of […] % of all households after […] seems aggressive and will only be possible through a massive ‘penetration pricing’ strategy shifting existing customers of other operators to the GNA network.

In relation to the wholesale prices charged by GNA to the wholesale operator, the Commission argues in the opening decision that although experts suggest that fibre networks entail lower operational expenditure than current copper telecommunications and cable networks, the GNA wholesale prices are still considerably lower than what market reports suggest.

The Dutch authorities argue that fibre networks entail lower operational costs and have a longer economic lifetime than existing networks therefore lower wholesale prices are possible compared to what data on existing networks might suggest. This cost advantage provides sufficient room for relatively low wholesale prices compared to the offers on current copper networks.

Regarding the validity of the investment cost figures, the Commission found in the opening decision that benchmark figures indicated that the capital expenditure per connection projected by GNA appeared to be low in comparison with data available from market players and other sources.

The Dutch authorities argue that the feasibility of the planned investment costs are further underpinned by the topology and the characteristics of the geographic area where the network is deployed: the areas concerned in Amsterdam have a high population density and many newly built or renovated and multi-household buildings that help to reduce the costs of the deployment of the network per household.

Regarding the appraisal of the residual value of the network, the Dutch authorities argue that the estimate in GNA’s business plan is realistic, as the economic lifetime of fibre networks can be 30 years or even more. Within this timeframe, no major additional investment or maintenance costs will be necessary, contrary to existing copper or cable networks. Furthermore, the authorities argue that the network in place will have significant ‘strategic value’ due to the ‘natural monopoly characteristics of fibre access networks’ that GNA will enjoy due to its first mover advantage.

The Dutch authorities also commented on the Commission’s preliminary conclusion that all assumptions underlying the business plan seemed optimistic and that there is a high degree of sensitivity for the success of the project if even one of the targets (such as penetration grade) does not materialize.

The main conclusion of the submitted study, shared by the Dutch authorities, is that the investment of the Amsterdam municipality is commercially viable and therefore in line with the MEIP.

First, the Dutch authorities reiterate their position that the doubts of the Commission regarding ‘concomitance’ and ‘identical terms and conditions’ originating from the pre-investments of the Amsterdam municipality have been properly addressed by the reimbursement of the relevant pre-financed costs by GNA. Furthermore, they claim that GNA’s business plan is feasible and realistic, therefore the investment of the Amsterdam municipality in the GNA project is fully in line with the MEIP.

The Dutch authorities argue that all parties providing comments in this case failed to take into account that the investments of private investors are sufficient to conclude the MEIP conformity of the investment. They also claim further that, according to the relevant Court jurisprudence, the analysis of the business plan was not necessary in the presence of these private investors.

For the reasons explained in recital 79, the Dutch authorities doubt the qualification of the four other companies as interested parties and are of the opinion that these parties only submitted general observations which are not relevant for the assessment of the measure at hand. Therefore, the Dutch authorities do not consider it necessary to comment these observations. The Dutch authorities also do not provide comments on the observations by third parties on the compatibility of any State aid contained in the measure as according to the authorities, a compatibility assessment is not necessary in the current case as no State aid is involved in the measure.

The Commission has examined whether the measure can be qualified as State aid within the meaning of Article 87(1) of the EC Treaty, which provides that ‘any aid granted by a Member State or through State resources in any form whatsoever which distorts or threatens to distort competition by favouring certain undertakings or the production of certain goods shall, in so far as it affects trade between Member States, be incompatible with the common market’. It follows that in order for a measure to be qualified as State aid, the following cumulative conditions have to be met: 1) the measure has to be granted out of State resources and be imputable to the State, 2) it has to confer an economic advantage to undertakings, 3) the advantage has to be selective and distort or threaten to distort competition, 4) the measure has to affect intra-Community trade.

In the present case, the investment by the municipality of Amsterdam was made jointly with two private investors, namely ING RE and Reggefiber. The Commission will therefore first examine whether the investment of the municipality of Amsterdam fulfils the market economy investor test due to the fact that it was made concomitantly with a significant private investment. For this purpose, the Commission will examine the following criteria:

First, it has to be identified whether these investors are market investors and whether the investments by the private investors have real economic significance. Such significance should be assessed in absolute terms (a significant portion of the total investment) and in relation to the financial strength of the private investor concerned.

Second, it has to be assessed whether the investment by all parties concerned take place at the same time (‘concomitance’).

Third, it has to be identified whether the terms and conditions of the investment are identical for all shareholders.

Subsequently, and at a subsidiary level, the Commission will also examine GNA’s business plan, in particular in view of the claims of the complainant Liberty Global/UPC and other interested parties, which argued that there is no feasible business case for the network built by GNA.

In absolute terms, the two private investors both invest a substantial amount (EUR 3 million, respectively) in the partnership GNA. If an investment of EUR 3 million, compared to the financial strength of both ING RE and Reggefiber, could be considered in relative terms to the size of the investors to be a small investment, such an investment is certainly significant in relative terms to the overall capitalisation of GNA and the capital contribution of the municipality of Amsterdam.

The Commission also notes that according to Dutch corporate law, one third of the shares are sufficient to form a blocking minority regarding any important decision of GNA. Therefore, the two private investors can jointly form a blocking minority within the company.

To conclude, both ING RE and Reggefiber are market investors and their investments have real economic significance both in absolute and relative terms if seen in the context of the shareholding structure of GNA.

The Commission noted that the municipality commissioned several studies in 2003 and 2004 to prepare the project. Furthermore, the municipality took initiatives which seem to go beyond these preliminary steps. Despite the absence of a firm commitment by private investors, the municipality published and organised tenders and even negotiated contracts for the construction and the exploitation of the network. In addition, the municipality of Amsterdam financed certain digging activities and purchased software for the construction of the network.

The new information received during the formal investigation enabled the Commission to establish the following facts: First, a substantial part of the activities and pre-investments (EUR […]) was explicitly agreed in the ‘Letters of Intent’ signed by the prospective shareholders of GNA and co-financed by all of them proportionally to their stake even before the establishment of the company, as all partners in the venture considered necessary to undertake individually and separately certain steps prior to GNA’s incorporation.

Second, all pre-investments (including EUR […] earmarked only by the Amsterdam municipality) were included in the business plan on which the investment was based and hence were agreed between all shareholders of GNA. Thus, all partners in the venture considered those pre-investments as useful steps prior to the establishment of GNA. According to the Dutch authorities, there was agreement among all shareholders that the portion initially financed by the municipality would be reimbursed by GNA. In other words, the municipality’s conduct did not pre-empt or influence the behaviour of the other market investors.

On the basis of the above, the Commission considers that the fact that the municipality of Amsterdam did carry out some limited pre-investments prior to the formal setup of GNA does not call into question the fulfilment of the MEIP given that there was agreement among all shareholders that the municipality of Amsterdam would have to be reimbursed for these pre-investments.

Based on the submissions by the Dutch authorities at the moment the formal investigation was initiated, the Commission was not in a position to calculate or verify the total amount of these ‘pre-investments’ which the Commission estimated to be in the magnitude of EUR 1,5 million. Furthermore, it was not fully clear to the Commission how those costs were shared between the shareholders and included in the business plan of GNA.

In particular, the Commission feared that the ‘pre-financing’ by the municipality — partly without the explicit agreement of some of the other investors — might have reduced the investment risk of the other investors in GNA and could have had a positive impact on their willingness to invest in GNA. The information submitted by the Dutch authorities following the opening of the formal investigation allayed these preliminary doubts.

Second, all costs related to the pre-investment were also initially included in the business plan of GNA, hence no new costs seem to have emerged after the signing of the GNA agreement that would have altered the terms and conditions for the other shareholders. This is in line with the finding that there was agreement among all shareholders that the municipality of Amsterdam would have to be reimbursed for the pre-investments carried out.

Third, although the municipality of Amsterdam took the lead and pre-financed part of the project costs, those initiatives and investments could not have reduced the risks involved in the project for the other shareholders. Contrary to the preliminary doubts raised in the opening decision, the Commission comes to the conclusion that the investments initially financed by the municipality in undertaking limited civil works and purchasing software could not, in view of their nature and their limited financial significance, have altered the risk profile of the project. The same is true for the pre-investments co-financed by all prospective shareholders in parallel to the signing of the ‘Letters of Intent’. The analysis of the business plan clearly shows that the business risks of the investment in GNA is linked to the success of the project in the years to come, particularly in terms of market evolution, and not to the very first steps preparing the project.

In view of this information, the Commission concludes that all shareholders in GNA have invested under the same terms and conditions.

UPC argued that ING RE might have decided to invest in the GNA project not on the basis of economic considerations, but rather as part of their marketing strategy to maintain a good relationship with the municipality of Amsterdam, which is allegedly an important business partner of ING RE.

The Commission’s own investigation and the information submitted by interested parties have not brought forward any elements indicating that the statement of the Dutch authorities is incorrect.

On this basis, the Commission concludes that the investment by the municipality of Amsterdam was made at the same time and in comparable circumstances as the significant capital contributions by the private investors.

Accordingly, the investment made by the municipality of Amsterdam is in line with the market investor principle and does not constitute State aid.

The Commission received comments on the business plan analysis contained in the opening decision both from the Dutch authorities and from UPC which enabled it to deepen its assessment.

The Commission notes that the business plan of GNA relates to a newly formed undertaking with no track record, acting in a new and innovative business segment (FttH technology, ‘three-layer model’, where passive and active infrastructures are operated and managed separately, with an open and non-discriminatory access offered to all retail operators, see description part recitals 21-30). Thus, in such a case, the assessment of a business plan of a newly formed undertaking is necessarily and inevitably based on future market projections and hypotheses regarding the likely evolution of demand and supply for FttH services.

GNA applied three main financial performance indicators to measure the success of the project being the cash-flow generation, the return on equity and the internal rate of return (IRR).

The Commission considers that the IRR ratio appears to be the most appropriate parameter for an analysis of the business plan. The IRR is used to make decisions on long-term investments and to compare different investment projects. The underlying IRR of GNA’s business plan is […] %.

In its submission, UPC argued that due to the novelty and the high risk involved in the project, the targeted IRR for GNA, which is basically a start-up firm, must be higher than the WACC figures of a well-established company with significant customer base and cash flow generation, such as KPN or UPC.

The Dutch authorities question the Commission’s assessment regarding the benchmarks used for the assessment of the IRR in the opening decision. They claim that the WACC figures are related to vertically integrated operators, while GNA is only investing into a passive network, which is more similar to an infrastructure investment for which lower rates of returns are generally required by investors.

The Commission finds that the targeted IRR in GNA’s business plan appears to be within the market expectations for companies active in the telecommunications market. In addition, the Commission recognises that the investment project under scrutiny is different from that of a vertically integrated operator and it presents characteristics of an infrastructure type investment, for which a lower IRR is required.

One of the most important factors for the business plan is the targeted penetration rate. As revenues for GNA will depend to a large extent on the achieved penetration rate, i.e. the percentage of connected households, the feasibility of achieving the targeted penetration rate is of crucial importance for the success of GNA’s business.

In contrast, the Dutch authorities argue that new services can be provided over the symmetrical fibre broadband connection (such as file sharing and other ‘peer-to-peer applications’, HDTV), which belong to a different market than the current asymmetrical connections. Furthermore, the Dutch authorities relying on the already mentioned study prepared by Stratix Consulting and Delft Technical University stress that several successful examples not only from the Netherlands, but also from the US and Japan indicate that the targeted penetration rate is realistic.

The Commission has assessed the arguments of the various parties in this respect. The Commission notes that GNA, in order to determine the penetration rate curve, […]. This penetration rate forecast model incorporates all the assumptions required, including take-up rates, speed of take-up rate and churn rates as well as those assumptions that were quoted by the UPC as being important factors to assess the feasibility of the business plan. Therefore, the business plan includes the relevant factors that are necessary for the assessment of the penetration rate.

On the question whether the penetration rates in the business plan are achievable, the Commission notes that it will depend to a large extent on the evolution of the market, the speed at which new applications and technologies requiring very fast, symmetrical fibre broadband connection will be adopted by service providers and the reaction of customers to these new possibilities. These factors cannot be known with certainty at this point in time, as is demonstrated by the different views between UPC (more sceptical regarding market prospects) and Reggefiber, ING RE and Delft Technical University (who have endorsed the estimates in the business plan either as investors or as independent consultants).

More specifically on the churn rates submitted by UPC to show that the project is failing to reach any meaningful penetration rates, the Commission notes that the submitted figures cover the period between 1 January 2006 and 1 June 2007, while retail operators using the GNA network started offering the services to customers in limited areas of Amsterdam only in March 2007. Given the very limited amount of time elapsed since services are provided over the GNA network, the Commission is not convinced that meaningful information could be elicited from the churn rates at this stage.

The Commission therefore concludes that it is conceivable for a market economy investor to invest in the project on that basis of the penetration rates foreseen in the business plan (indeed, this is what Reggefiber and ING RE did).

Wholesale prices per connection charged by GNA to BBned for the exploitation of the passive network […].

In its submissions, UPC has calculated that GNA has to charge at least EUR 20-EUR 22 per month for a wholesale connection enabling triple-play services on its network. However, at this price level, the final retail service prices would necessarily be more expensive than current similar offers of the existing operators, which allegedly raises doubts about the targeted penetration rate.

In contrast, the Dutch authorities argue that the new fibre technology requires different cost calculations than the traditional copper or cable lines. For instance, the fibre network requires far lower operational expenditures (such as maintenance, management costs) and also has a longer economic life, i.e. a longer amortisation period (up to 30 years).

As regards the prices charged by GNA for the wholesale access, there are some indications that fibre networks may entail lower operational expenditure than legacy telecommunication and cable networks. Based on these considerations and also taking into account the benchmark information available and the results of the Stratix Consulting/Delft Technical University report, the Commission concludes that the wholesale prices in the business plan are not unrealistic compared to similar services provided by other operators.

Considering also the topography of the areas (densely populated area on a flat terrain), the fact that the civil engineering companies carrying out the works accepted to do them for a price compatible with the business plan, and the available benchmark data, the Commission finds that the planned GNA investment figures appear to be realistic. The Commission also takes note that GNA calculated with a certain level of buffer in case of an overrun of the investment costs which is in line with prudent market investors’ practice and provides further evidence for the robustness of the estimates of the investment costs.

The estimated residual value of the passive network has a pivotal role in GNA’s business plan to achieve the financial targets and to provide a collateral for the investors. GNA applies a multiple-based calculation to determine the residual value of the asset (the projected value of the network in […] is EUR […]), the value is depending only on the achieved penetration rate. The Commission also assessed with an alternative multiple-based valuation the residual value of the GNA network, resulting in a value range of EUR […] million at […] % penetration rate, which matches GNA’s estimate.

The Dutch authorities argue that the calculation of GNA’s business plan in relation to the residual value of the network is realistic and based on a correct methodology. In addition, they assert the economic lifetime of fibre networks can be […] or even more. Furthermore, they assert that the network in place will be valuable due to its first-mover advantage and because the construction of a second similar network might not be economically viable in view of certain natural-monopoly characteristics of fibre access networks. These latter factors allegedly provide further evidence that the network in place will have significant value even if the business plan does not fully materialize.

In the opening decision, the Commission also raised certain preliminary methodological concerns regarding GNA’s business plan. For instance, corporate tax is not included in the business plan. The Dutch authorities argue that the shareholders of GNA chose the legal form of ‘gesloten commanditaire vennotschap’ that has no obligation to pay profit tax. Therefore the results of GNA will be consolidated directly by its shareholders and the project is assessed on a ‘pre-tax base’.

UPC also stressed that the Commission should take into account not only the individual assumptions but the interrelation between them. For instance, UPC argues that high levels of penetration with high prices together are considered as impossible. The Commission has assessed the methodology and the figures on which the business plan is based and found that they can be considered acceptable to a private investor operating under normal market economy conditions.

UPC also argues that in its calculations about the GNA business plan, it did not take into account that GNA will provide rebates for the users of the network in the first years, as this information was revealed in the Commission’s opening procedure. UPC argues that such contribution by GNA to the marketing costs of the complete project further deteriorate any financial return of the project for the investors and provide further evidence that the GNA business plan is not feasible. In this respect, the Commission notes that it is normal market practice that new services are offered at discount prices in the beginning in order to reach a certain customer base. Furthermore, the financial impact of those rebates was fully taken into account in the GNA business plan, which was analysed by the Commission.

After the formal investigation and having assessed the additional information received, the Commission comes to the conclusion that the GNA business plan is in line with the MEIP.

The business plan is based on the main forecast that the evolution of the telecommunication and media markets in the Netherlands will translate in significant demand for high speed broadband services, which will be to a large extent be satisfied by FttH networks. From this forecast, which has been endorsed by the report of Stratix Consulting/Delft Technical University, derive the assumptions regarding prices and penetration rate of the GNA network. Together with other assumptions (e.g. investment costs), these factors drive the result that the project will sufficiently remunerate its investors.

The Commission has assessed the plan and the assumptions therein by benchmarking it with comparable projects wherever possible, by checking its internal consistency and the feasibility of the assumptions. The conclusion from this assessment is that the business plan is methodologically correct and takes into account all the relevant factors that may impact on the success of the project.

Furthermore, the Commission finds that GNA’s business plan does not contain manifestly erroneous assumptions. The assumptions underlying the plan are realistic if seen against the main forecast on the evolution of the telecommunications and media markets. They also appear realistic when benchmarked against comparable projects. The reservations that may be raised against some of the assumptions of the business plan as a matter of principle or starting from a different forecast about the future evolution of the relevant markets are not sufficient to undermine its overall credibility. Such divergence of views pertains to the wide margin of judgment that comes into entrepreneurial investment decisions.

Having these elements in mind, the Commission concludes that a private investor operating under normal market economy conditions could invest in GNA on the basis of its business plan.

As regards the submissions of UPC, ONO, FT, COM HEM and the anonymous party, asking the Commission to adopt a strict line regarding the application of the MEIP in the present case in view of the alleged ‘precedent character’ of the project for other broadband investments in Europe, the Commission wishes to highlight that the MEIP assessment always has to be conducted on a case-by-case basis in line with the existing case-law and its decision-making practice in this field.

Overall, the Commission therefore concludes that the investment by the municipality of Amsterdam does not constitute State aid since it was made at the same time as a significant capital contribution on the part of a private investor made in comparable circumstances. In addition, an examination of the business plan has equally confirmed that the investment is in accordance with the Market Economy Investor Principle.

Following the opening of the formal investigation procedure, the Dutch authorities addressed the preliminary doubts expressed by the Commission in the opening decision in a satisfactory manner. In particular, all pre-investments by the Amsterdam municipality, which were one of the main concerns of the Commission in the opening decision, were reimbursed by GNA. The Commission finds that the municipality of Amsterdam invests in GNA on the same terms and conditions as the private parties involved in the project, which are investing on the basis of GNA’s business plan.

Consequently, the Commission concludes that the investment of the municipality of Amsterdam in GNA does not constitute State aid within the meaning of Article 87(1) of the EC Treaty as it is in conformity with the Market Economy Investor Principle,

HAS ADOPTED THIS DECISION: